The major credit card issuers have various policies in place to crack down on those who apply for credit cards exclusively for welcome offers. While credit card issuers sometimes have big bonuses to get customers to apply, they do so with the hope of people holding onto a credit card long term. While it’s understandable that sometimes a card might not work out for someone, those who constantly open and close cards may find themselves facing some restrictions.

In the case of American Express, the issuer has a policy of only letting you earn the welcome offer on a card “once in a lifetime.” Anecdotally a “lifetime” in this context typically refers to a period of around seven years, though that policy isn’t published. So if you’ve had a card before, you won’t generally be eligible for the welcome offer on the card again.

In the case of American Express, there’s a pop-up that has been showing up during the application process for some people for the past few years, so I wanted to cover that in more detail.

In this post:

What is the Amex application pop-up warning?

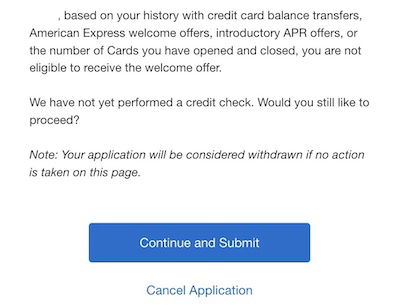

During the American Express application process, you might see that you’re faced with the following pop-up:

Based on your history with credit card balance transfers, American Express welcome offers, introductory APR offers, or the number of Cards you have opened and closed, you are not eligible to receive the welcome offer.

We have not yet performed a credit check. Would you still like to proceed?

Note: Your application will be considered withdrawn if no action is taken on this page.

This will typically appear after you enter your personal information and submit your application. As the message states, there’s the potential that you won’t be eligible for the welcome offer on the card that you applied for.

This means you could still apply for the card and simply not receive the bonus. But this also gives you the option to cancel your application, so that there’s no credit pull (separately, Amex also has an awesome “Apply with Confidence” feature on some cards).

What causes the Amex application pop-up warning?

There are several reasons you could potentially be faced with this pop-up warning during the application process.

You could get this message because you’ve applied for this card in the past, and just didn’t remember. In this case I’d consider the message to be genuinely helpful and a great feature, since you’re able to avoid a hard pull for a card where you won’t get the bonus.

Under other circumstances this can be a bit more confusing, though. The warning officially states that you could be ineligible due to one of four reasons:

- Your history with credit card balance transfers

- Your history with Amex welcome offers

- Your history with introductory APR offers

- Your history with the number of Amex cards that you’ve opened and closed

Suffice it to say that this is vague. What does all of this mean in practice? I’d say the most likely reasons you’d be faced with this message is the following:

- Even though you may technically be eligible for a welcome offer based on not having had that exact card before, Amex may decide that you’ve had too many cards in that same card “family,” and maybe canceled too many of them too quickly, didn’t spend enough on them, etc.

- Maybe Amex feels you have opened and closed too many cards with the issuer, and/or haven’t spent enough on the cards for it to make sense to approve you for another bonus

- If you’ve engaged in any sort of other behavior that Amex frowns down upon, Amex may decide not to offer you a welcome bonus on a particular card

One other interesting twist is that sometimes these pop-ups are specific to certain “families” of cards. In other words, you may get this message when applying for a Hilton Honors Amex you’ve never applied for before, while you may not get this message when applying for an Amex Platinum Card.

Is the Amex pop-up warning becoming more common?

While I don’t have any data, anecdotally it sure seems to me like there are more and more reports of these pop-up warnings, even for situations where you wouldn’t expect them.

I think most of us can understand why Amex would want to restrict people who repeatedly open and close cards, without keeping them for a long time and spending money on them. However, I’m increasingly seeing data points of people getting this warning even though they only have a few Amex cards, have had them open for years, have never even had a card in the same family, etc.

So while I don’t have an explanation as to what is causing this, know that you’re not alone if you’re finding yourself getting the pop-up warning even if you’re a good Amex customer.

Is there any way to get around the Amex application pop-up warning?

If you’re faced with this pop-up during the application process, is there anything you can do? Yes and no.

No, there’s no one you can (realistically) contact to appeal this warning, and there’s no way that you’ll get this removed from one minute to the next. For whatever reason Amex has decided you shouldn’t be eligible for a welcome offer on a particular card, and that’s that.

The good news is that just because you get this message once, doesn’t mean you’re locked out of earning welcome offers forever. While there’s no magic formula, here are some things to consider doing:

- Avoid applying for Amex cards for some significant amount of time (maybe a few months, at least); I’d assume Amex is tracking how often people apply for cards, so don’t submit an application every few days to see if the pop-up still shows up

- If you have a lot of open Amex cards you’re not spending money on, put some spending on those cards to show some activity

- Since these restrictions are often specific to “families” of cards, after a few months maybe try applying for a card in a different “family,” to see if you have the same message (it’s also possible you might not get a message like this if you applied immediately for a different card, but I’m trying to recommend a conservative approach here)

Like I said, there’s no consistent way to get this resolved. Assuming you’ve never had a particular card before, Amex has probably decided that something about your current relationship with the company isn’t ideal, and try to adjust things accordingly.

Bottom line

Amex has a pop-up warning during the application process, which will tell you if you’re not eligible for the welcome offer on a card, prior to even pulling your credit. This is helpful if you’re not sure if you’ve had a card before, given Amex’s “once in a lifetime” application rule.

But Amex isn’t just using this pop-up in situations where you’ve had a particular card before, but also sometimes in situations where the issuer has simply decided that you shouldn’t get the bonus on a card. This can happen for a variety of reasons, and the best way you can deal with it is by continuing to spend responsibly on your Amex cards, and not applying for other Amex cards for a while.

Have you ever dealt with Amex’s pop-up warning? If so, what was your experience?

In October I tried for the Hilton aspire and got the popup, even though I have had AMEX cards for two decades. I knew I wanted another card though, so I decided which cards I would try for and a few days later tried again. I first tried for the Hilton aspire and got the popup. I immediately then tried for the green card and got the popup. A few seconds later I applied for the Gold card and got it with 75K bonus points. The points recently hit my account.

I had my first Amex green at college fair in 1996 with no SUB. This account was later closed, re-opened in '01 and closed in 2004 going to Citi and Chase. As of 2017 I decided to go back to Amex and have since opened Gold, BCP, Delta Gold, Hilton Aspire-all with SUB and all renewed with heavy spending and usage. I recently accepted the offer to upgrade to Delta Platinum for 30K points for...

I had my first Amex green at college fair in 1996 with no SUB. This account was later closed, re-opened in '01 and closed in 2004 going to Citi and Chase. As of 2017 I decided to go back to Amex and have since opened Gold, BCP, Delta Gold, Hilton Aspire-all with SUB and all renewed with heavy spending and usage. I recently accepted the offer to upgrade to Delta Platinum for 30K points for $3K spending. I don't have a record of opening accounts for SUB and my first card was a basic Green Amex from 27 yrs ago in good standing. I have tried every year to get the Platinum card with SUB and get denied. Sept 9, Amex sent me an offer saying I was pre-approved (Finally!!!!) for Platinum for 75k points and $6,000 spending. I filled application and got the same popup. My FICO is high and I even get auto-CLI on my other cards so I'm baffled why I'm not eligible for platinum SUB after 10 attempts and a solicitation. I'm stuck being an additional card holder on my husband's account and 90% of charges are on my addn'l user card.

I tried to apply for the Marriott Brilliant AMEX, from everything published I should be eligible for the welcome bonus. I have two other Marriott cards, but one is a business card and the other is the old SPG Amex (not luxury) from everything I read, I should be eligible but got the "no welcome bonus" pop-up.

I was trying to book some tickets on delta airlines website when I got a pop up to apply for delta gold Amex with a 70,000 bonus and no annual fee for first year, which I did not need or want but since I was about to spend 3k on a hotel I said why not? Got no pop up, was approved. After completing the bonus, no miles showed up for few months. When I...

I was trying to book some tickets on delta airlines website when I got a pop up to apply for delta gold Amex with a 70,000 bonus and no annual fee for first year, which I did not need or want but since I was about to spend 3k on a hotel I said why not? Got no pop up, was approved. After completing the bonus, no miles showed up for few months. When I called them they said the offer was declined. I recently closed the Amex platinum after having it for 8 years and switched to business platinum as I started a new business. Never had any delta card and never closed any card within a year of having it. Perplexed to say the least. Amex being unhelpful and saying it's in the terms and conditions but no specific answer.

I had a gold amex delta card. At the airport the lady at the ticketing counter talked me into opening a platinum card because right now there is a 85,000k welcome bonus skymiles. I told her I already have the gold amex. She said this is a different card so I will get the welcome bonus for this card if I am approved for the card. It’s a $250 annual fee but I felt it...

I had a gold amex delta card. At the airport the lady at the ticketing counter talked me into opening a platinum card because right now there is a 85,000k welcome bonus skymiles. I told her I already have the gold amex. She said this is a different card so I will get the welcome bonus for this card if I am approved for the card. It’s a $250 annual fee but I felt it was worth it to get 85k points , plus she said I will get a free companion pass every year.

We’ll come to find out u have to pay the annual $250 right when u open it and don’t receive a companion pass untill u pay another yearly fee another $250 next year. To sweeten the bait and switch I never got the 85k points and when I called they said it’s because I already had a gold card. I was escalated twice to 2 managers that made me feel like a criminal and had no empathy. Or any offer of some mortgaging points or any type of customer service solution . It was a completely unethical bait and switch. I wish I had never upgraded to a higher tier card. As an Amex card holder for 9 years I am utterly disappointed in their lack of regard and value for loyal customers.

found this posting after landing in pop-up jail... I have 2 AMEX's right now, a delta one (2018) and a hilton one (2019). Have not applied for any amex's since, but I did threaten to close the delta one this summer and they gave me a retention bonus. So perhaps that was a mitigating factor as I tried to open the Green card today to take advantage of the lushious bonuses. womp womp. i'll keep trying i guess.

Just had this happen when applying for a Delta Skymiles Gold for a 65K bonus. I have 3 other amex cards. a Blue Cash Everyday and Amex everyday card that I have had for over 10 years and a Hilton Honors rewards that I opened 5 months ago. I have an 830 credit score, have done some other non amex sign up bonuses but haven't canceled any cards in the last 2 years. Disappointing.

I applied for the platinum amex card for the 150K bonus points and was accepted. I checked to see where the points were after spending the required amount of $$ in the required amount of time and they told me that I received this "decline offer" message upon application. I would not have continued if I saw that message. I think there was a glitch in their system. To say that I am angry after 3 months of spending on that card for the points is an understatement.

Just happened today. I have three AMEX (Platinum, AU on wife's Hilton Business, and an old Freedom Business that doesn't get used). Was told today that I don't qualify for the Hilton Surpass welcome bonus. Great 20 year relationship with AMEX so no clue why this is....

Same thing here. Applied for Schwab Amex and got the popup. Only Amex I have is the Basic Hilton Amex which I have had for years.

I've tried applying four times for the Green Card with the elevated welcome bonus (60k and 20% off eligible travel/transit). Each time I get the vague pop-up. When I called the reconsideration line, they told me this specific welcome offer is good for new Amex customers only. I already have the Platinum and Delta Platinum so therefore I was not eligible for this offer. I could have the card if I wanted but no welcome...

I've tried applying four times for the Green Card with the elevated welcome bonus (60k and 20% off eligible travel/transit). Each time I get the vague pop-up. When I called the reconsideration line, they told me this specific welcome offer is good for new Amex customers only. I already have the Platinum and Delta Platinum so therefore I was not eligible for this offer. I could have the card if I wanted but no welcome offer, or at least not this welcome offer anyway. I was told to watch for future welcome offers that might include existing Amex customers and apply then.

Has anyone else been given this reasoning when getting the pop-up? I can't find that "rule" anywhere in the application for the Green Card. I wonder if this same logic applies to other people getting the same pop-up regardless of what card they apply for.

I got popup jail, and I’m guessing it’s because I closed my personal gold card and kept the business gold. I spend a ton with Amex if you count business spend and none of the cards go unused. I’ll try again when the Green Card 60k offer is about to end.

just applied for the hilton surpass card and got the pop up, i only have the blue rewards card thats about 4 years old and i use pretty often with no balance so IDK why i got the popup

just got the dreaded pop up trying to get the Hilton bonus, I’ve not tried to get an Amex personal card since 2018. Have accounts over 10 years.

After calling they told me I canceled a card before 12 months in 2020.

I downgraded Hilton aspire to the free card and signed up for platinum in 2020. I never got the free card in the mail for some reason and did not activate...

just got the dreaded pop up trying to get the Hilton bonus, I’ve not tried to get an Amex personal card since 2018. Have accounts over 10 years.

After calling they told me I canceled a card before 12 months in 2020.

I downgraded Hilton aspire to the free card and signed up for platinum in 2020. I never got the free card in the mail for some reason and did not activate it. Totally forgot about the card as it never added to my profile.

So because the card I never got auto canceled I’m no longer eligible for bonus

I just got the dreaded pop up trying to get the Hilton bonus, I’ve not tried to get an Amex personal card since 2018. Have accounts over 10 years.

After calling they told me I canceled a card before 12 months in 2020.

I downgraded Hilton aspire to the free card and signed up for platinum in 2020. I never got the free card in the mail for some reason and did not...

I just got the dreaded pop up trying to get the Hilton bonus, I’ve not tried to get an Amex personal card since 2018. Have accounts over 10 years.

After calling they told me I canceled a card before 12 months in 2020.

I downgraded Hilton aspire to the free card and signed up for platinum in 2020. I never got the free card in the mail for some reason and did not activate it. Totally forgot about the card as it never added to my profile.

So because the card I never got auto canceled I’m no longer eligible for bonus

Does this mean I will be denied the card?

I received the pop up when applying for Schwab Platinum and immediately was approved for a 200k Amex Biz Platinum and Biz checking bundle offer. Then 6wks later applied for Amex Green (personal) and got the pop up again. On the same day, I received via mail and app a targeted Amex Biz Plat offer for 155k.

I got the pop up today when I applied for the platinum and have no clue as to why. I’ve had my Gold for two years and have never had the platinum. It’s a 125K bonus +$200 statement credit referral offer. I’m pretty bummed out about it.

I just had this happen to me with the new Green bonus. Got the dreaded pop up. I have three Amex cards - Plat, Hilton no fee and everyday. Been with Amex since 2019 and have never applied for the Green before.

Same here, just got it on the Green bonus...I've never had the green. I currently only have a Gold Card and a no fee every-day card I've had both for years...and I put a lot of spend on the Gold card so doesn't seem to be due to inactivity or quick-closes.

So weird I got the pop up for the green. Just opened plat and gold 2 weeks apart and got both subs in March- April. I Have put over 30 k between cards and have paid them all off . Maybe they don’t like that I am maximizing my spend , and a customer that cost them money . Only spending on flights on plat. And food and groceries on gold lol.

I called before I tried for the green card 3 weeks ago. Agent couldn’t tell me when I asked about SUB - I had opened it more than 50 years ago before SUB’s, and converted to Gold about 7 years ago. I closed Gold when I went to platinum 3 years ago and routinely spend along with my amex business cards. But still got pop-up jail.

just a brief reminder

My P2 has been getting this pop-up for years. She has never closed an Amex card! She has one business and one personal card with them (both Marriott, open 4 and 5 years for status boost/free nights) as well as a corporate green card and is authorized user on her father's Gold card (oldest account). We spend nearly zero on all cards except the corporate card which is just for work expenses. Meanwhile, they keep...

My P2 has been getting this pop-up for years. She has never closed an Amex card! She has one business and one personal card with them (both Marriott, open 4 and 5 years for status boost/free nights) as well as a corporate green card and is authorized user on her father's Gold card (oldest account). We spend nearly zero on all cards except the corporate card which is just for work expenses. Meanwhile, they keep approving me for bonus after bonus despite having had, and mostly closed, nearly two dozen cards over the years. I'm pretty sure activity plays a big role.

What's a P2?

I realize my comment will be taken as heresy on OMAAT. Card issuers have come to realize that some applicants have been gaming the system by churning cards just to gather points or miles. While not illegal the system is being revamped to reward card use rather than churning. I see nothing wrong with that.

I got the pop up when applying for the Amex Green. I have the Platinum, 3 years, and Gold, 1 year, and received bonuses on both. I have also received the bonus for a Amex business checking account. Was hoping to get the 60k and new Green card.

I got the pop-up yesterday applying for the Green Card via referral. I tried secure chat from my account just to be given a phone number, the phone rep couldn't tell me anything about why no bonus, there was literally nothing she could do to help me out. I even asked if I applied over the phone could she tell me why no bonus eligibility... The answer was no, sorry. It's very confusing and must...

I got the pop-up yesterday applying for the Green Card via referral. I tried secure chat from my account just to be given a phone number, the phone rep couldn't tell me anything about why no bonus, there was literally nothing she could do to help me out. I even asked if I applied over the phone could she tell me why no bonus eligibility... The answer was no, sorry. It's very confusing and must be my spending habits, I have never held the Green card, I only have a handful of cards, my last Amex card app was more than 5 years ago. Guess I'll go find a different card that i can get a bonus on...

Experiences vary widely. I've "solved" the dreaded popup with a couple thousand spend, on one card, over two months. But I've also had it stick for almost a year. Colleagues have reported that a few hundred spend monthly on two cards, for four months, cleared it. It's clearly in Anex's interest to keep this issue vague.

There are no recent data points of spend actually helping - that appears to be advice from a few years ago and they've tweaked their algorithm since then. What definitely is true is that the pop up criteria is different for each individual card and for elevated bonus offers associated with each card. The current plat and gold top offers (150k/90k +$200 statement credit) are really notorious for giving almost everyone the pop up, but...

There are no recent data points of spend actually helping - that appears to be advice from a few years ago and they've tweaked their algorithm since then. What definitely is true is that the pop up criteria is different for each individual card and for elevated bonus offers associated with each card. The current plat and gold top offers (150k/90k +$200 statement credit) are really notorious for giving almost everyone the pop up, but other elevated offers for the same cards (125/75) are easier to get.