I’m a fan of both the The Platinum Card® from American Express and The Business Platinum Card® from American Express. At the moment I have the Amex Personal Platinum Card, while Ford has both that and the Amex Business Platinum Card.

I’m reconsidering my overall strategy with these cards, though, given the announcement last week that the Amex Business Platinum Card will no longer offer a 50% rebate on Pay With Points redemptions. This was an opportunity to get two cents of value per point, which I’d consider to be the very best use of any transferable points currency.

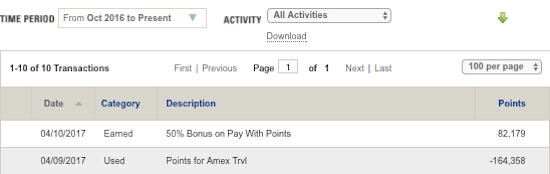

As of June 1, 2017, that rebate was cut to 35%, meaning that you’re getting about 1.54 cents per Membership Rewards point, rather than two cents. Furthermore, you’ll be limited to being rebated 500,000 points per year.

That’s still a solid return, but not quite as good. The good news is that if you opened the Amex Business Platinum Card between October 2016 and May 31, 2017, Amex will honor the 50% refund with unlimited points for one full year from the date your card was issued. So for many people it could still make sense to apply for this card by May 31, so you can maximize this opportunity before it’s eliminated.

With that in mind, what does this change mean for which cards I hold onto in the future?

The Amex Personal Platinum Card still pays for itself

The Amex Platinum Card has a $695 annual fee (Rates & Fees), though the benefits more than justify the annual fee, in my opinion. For one, the card offers a $200 annual airline credit and a $200 annual Uber credit, which I value at pretty close to face value. To be conservative, let’s just say the two combined are worth $350.

In addition, I receive the following:

- Access to Amex Centurion Lounges

- Access to Delta SkyClubs when flying Delta

- The ability to add authorized users for $195

- 5x points on airfare purchased directly with airlines on up to $500,000 on flight purchases per calendar year and then 1x

- up to $189 back on a CLEAR Plus membership every year

I do love access to Amex Centurion Lounges!

Let me focus on the above benefits, and we’ll leave out the other benefits that people might value, like Hilton status, car rental status, access to Amex Fine Hotels & Resorts, etc. I easily value the lounge access alone at $200, and would also probably pay the annual fee for 5x points on airfare alone. I spend quite a bit on airfare, so earning 5x points on that really lets me supercharge the points I can earn. (Enrollment is required for select benefits)

The Amex Business Platinum Card ($695 annual fee (Rates & Fees)) doesn’t offer 5x points on airfare (except airfare booked through Amex Travel), so to me, that’s a unique selling point of the personal card.

Is the Amex Business Platinum Card still worth it?

To me, the 50% refund on Pay With Points redemptions was a reason to potentially have both the personal and business version of the card. That’s over $1,000 worth of annual fees for the two cards, but you are also getting a lot of benefits out of it.

However, with this most recent change, I’m not quite as sure it makes sense to have both cards. Here’s the thing — ~1.54 cents of value per Membership Rewards point towards the cost of airfare is still pretty good. It’s marginally better than the up to 1.5 cents towards airfare that you get with Ultimate Rewards points. However, is it so good that it’s worth paying an annual fee on a card just to have access to it?

I’d say not. ~1.5 cents is right at the limit of where I wouldn’t be able to decide whether I’d rather have those points be “good as cash” towards the cost of a ticket, rather than transfer them to a partner. Some will still find it worthwhile, though with this change I probably wouldn’t go out of my way to hold onto both the personal and business version of the card.

Bottom line

There’s a lot of value to be had with the Amex Platinum Card and Amex Business Platinum Card.

At the moment I have the personal version of the card, value it immensely, and plan on continuing to use it (and paying the annual fee). The way I view it, the card costs me no where near the list price annual fee per year out of pocket, and for that, I get 5x points on airfare, Centurion Lounge access, Delta SkyClub access, and much more.

As far as the business version of the card goes, I was thinking of picking the card up soon, and Ford has it right now as well. I’m probably not going to pick it up anymore since I don’t see all that much value in having both cards, and I suspect Ford will cancel his when the annual fee comes due as well. Getting ~1.54 cents of value per point is still pretty good, but in and of itself isn’t enough reason to keep the card.

How will your Amex Platinum Card strategy change as a result of the recent change on the business card?

The following links will direct you to the rates and fees for mentioned American Express Cards. These include: The Business Platinum® Card from American Express (Rates & Fees), and The Platinum Card® from American Express (Rates & Fees).

One area no one has mentioned is the offers available on the Platinum. In the past two weeks I've redeemed a $35 credit on a $175 Hilton Garden Inn stay and used both my husband and my credits to get $100 credit on a $500 Norwegian Cruise deposit x2. Plus we can get $200 onboard credit by booking the cruise on the Amex Plat (via American Discount Cruises). I get some of these offers on...

One area no one has mentioned is the offers available on the Platinum. In the past two weeks I've redeemed a $35 credit on a $175 Hilton Garden Inn stay and used both my husband and my credits to get $100 credit on a $500 Norwegian Cruise deposit x2. Plus we can get $200 onboard credit by booking the cruise on the Amex Plat (via American Discount Cruises). I get some of these offers on my Hilton Surpass Amex but there are unique ones so that between the airline credit (SWA gift cards & fees), uber credits, and random deals, I get more than the $550.

And then get 50% ponts back (if I get the business platinum before May 31st)?

BTW, the offer is 150K points for 20K spend.

Can you combine points from gold and business platinum?

@ Rocky -- Sure can!

100K says:

May 4, 2017 at 4:15 pm

I just closed my Mercedes-Benz Platinum (Monday) and now am thinking of going for the Charles Schwab Platinum, which has a higher bonus right now (60K). How is Amex on closing and then applying so quickly, in your experience?

I have had 5 amex platinum cards (personal, MB, Morgan Stanley, Charles Schwab and business in the last 12 months). You should have no problem getting...

100K says:

May 4, 2017 at 4:15 pm

I just closed my Mercedes-Benz Platinum (Monday) and now am thinking of going for the Charles Schwab Platinum, which has a higher bonus right now (60K). How is Amex on closing and then applying so quickly, in your experience?

I have had 5 amex platinum cards (personal, MB, Morgan Stanley, Charles Schwab and business in the last 12 months). You should have no problem getting approved after closing one recently. Give it a try and if you are able to meet the spending requirements and get the points posted, you can cancel that card get refunded as well (within a month after the annual fee posted). I canceled all my platinum cards except Morgan Stanley due to one free AU card I use for my wife.

Interesting read. Personally I dropped this card when the annual fee came around. The tax to transfer to US airlines is annoying, Centurion lounges are sooooo overcrowded it's not even funny and I find UR points more valuable than MR right now. Though I can get how it could go the other way. All the hoops you have to jump through to get your airline credit, just not worth it to me.

It sucks but a lot of my invoices are $5k plus which gets 1.5 also my vendors are "small businesses which gives me another 2x for shop small. That still adds up to quite a bit so I will spend but just more selectively.

I agree with Kyle. AMEX is targeting luxury travelers that travel frequently. By emphasizing Uber, they want to appeal to millennials who could become long term Platinum users. If they become everyone's card, what little exclusivity is left out (read crowded lounges) will soon be lost.

I travel a lot and I use uber a lot too BUT outside the US. Since the card only covers uber rides within the US this was the ONLY reason I didnt sign up.

Penfed has a new card with 2% cash back and no annual fees. I got that one instead.

I agree with @adamh. I spend a fair amount on airfare, so I run that on my personal platinum and only have the biz platinum for the refund, to juice the return on my airfare spend. While I could spend $150 on CSR and get 1.5% redemptions on paid travel, that doesn't do much for me on the Membership Rewards front, and I'm quite certain I am better off earning at 5x and burning at...

I agree with @adamh. I spend a fair amount on airfare, so I run that on my personal platinum and only have the biz platinum for the refund, to juice the return on my airfare spend. While I could spend $150 on CSR and get 1.5% redemptions on paid travel, that doesn't do much for me on the Membership Rewards front, and I'm quite certain I am better off earning at 5x and burning at 1.54 cents (capped) than earning at 3x and burning at 1.5 cents (uncapped).

I haven't been invited, but if i were, i would seriously consider the Centurion Business card. Here's my thinking (would love others' thoughts on this): even at $2,500 / year (setting aside initiation fee), if you can redeem on any airline, in any class of service and get 50% back uncapped, the math seems to work. If you spend $7k on airfare on centurion, you get back an incremental 105,000 MR points and at $0.02/MR that's $2,100 of incremental value, which in my mind makes up the fee differential. If you have a business and can fund employee travel this way, seems like a no brainer, no? I've spent north of $20k on employee travel year to date (all funded by Amex biz plat) but were anchored to our selected airline for economy fares. Am I thinking about this right?

At the current set-up of X plat

1) I use it the first year to harvest all the benefits and then plan to cancel.

Not worth the $550 'membership' fees.

2) If they offer plat to me again without the once-per-lifetime language I will sign up again

and follow 1) LOL

I've come to the same conclusion - I have both, and I use the Business Platinum for, well, business expenses, and the Personal Platinum for, well, personal expenses. I'm going to use one of my additional cards on the Personal Platinum for business expenses so that I can track them separately.

My only hesitation is that my Business Platinum is my oldest card (many, many, many years), so I hate to lose the history, and...

I've come to the same conclusion - I have both, and I use the Business Platinum for, well, business expenses, and the Personal Platinum for, well, personal expenses. I'm going to use one of my additional cards on the Personal Platinum for business expenses so that I can track them separately.

My only hesitation is that my Business Platinum is my oldest card (many, many, many years), so I hate to lose the history, and would want to downgrade it to something.

Any suggestions?

The Uber credit is not worth face value, even for those of us who live in Uber cities. If it were a straight $200 annual credit, sure, but this goofy $15 a month crap they came up with will surely (as no doubt intended) cause breakage. I figure it's worth $100, enough to cover the increased fee, but no more than that.

They want the big traveler market more than they want the "big dining out" market or the "heading to the store" market. The Platinum is completely centered around big travelers. That's what the perks are centered around (the only transferable currency card that offers hotel status, for example). The airline bonus is just part of that overall strategy.

The idea here being that if someone has a lot of money, preferably, and travels a lot...

They want the big traveler market more than they want the "big dining out" market or the "heading to the store" market. The Platinum is completely centered around big travelers. That's what the perks are centered around (the only transferable currency card that offers hotel status, for example). The airline bonus is just part of that overall strategy.

The idea here being that if someone has a lot of money, preferably, and travels a lot it's the ideal card for them to carry. If it meets that, most people aren't us and probably don't have 4 cards they use, let alone 14 (guilty! I think it's 14?). If they want one card to use, they may as well use that one for other things that make Amex a profit, and that's the idea. You can criticize the strategy, but they seem pretty committed to that strategy. They don't want it to be everyone's everything card, they want it to be a specific market segment's everything card and likely nobody on this blog is in that segment. We play the game too well.

*Typed on GoGo internet over the Atlantic on a free pass from my Amex Platinum on tickets bought with Sapphire Reserve points and headed to a hotel paid for with by the bonus nights on the Hyatt card as well as the rest of the points off the Reserve card, transferred to Hyatt. Oh, and we're in upgraded seats courtesy of the airline credit off the Citi Prestige card. Yes, I have a problem...

I'm piling on here, but I can't understand how anyone would feel the AMEX Centurion Lounges are a benefit given they have turned into overcrowded feeding frenzies. As Lucky noted a few posts ago, quiet spaces found in the terminal with WiFi are a much better option for those of us trying to work.

As mentioned here many times, AMEX could improve this by limiting the number of guests of card holders either through...

I'm piling on here, but I can't understand how anyone would feel the AMEX Centurion Lounges are a benefit given they have turned into overcrowded feeding frenzies. As Lucky noted a few posts ago, quiet spaces found in the terminal with WiFi are a much better option for those of us trying to work.

As mentioned here many times, AMEX could improve this by limiting the number of guests of card holders either through issuing a set number of coupons or limiting all together.

I'm confused. If you got Biz Plat now you'd get the rebate for 13 months? Is that worth $450 annual fee to you?

I'm assuming your still using the AMEX Everyday Preferred for the 1.5X points on everyday spend?

@Lucky -- I'm with @The Oracle on this one.

Amex Platinum has structured their benefits to only appeal to heavy duty travelers. I know you are definitely part of this 99th-percentile travelers group, but for the "average Joe" credit card holder in the USA who flies once or twice a year, the financial math doesn't add up for the Platinum card (but still works out fine for the Sapphire Reserve).

Specifically, Amex is screwing up...

@Lucky -- I'm with @The Oracle on this one.

Amex Platinum has structured their benefits to only appeal to heavy duty travelers. I know you are definitely part of this 99th-percentile travelers group, but for the "average Joe" credit card holder in the USA who flies once or twice a year, the financial math doesn't add up for the Platinum card (but still works out fine for the Sapphire Reserve).

Specifically, Amex is screwing up big time by not giving a higher bonus (say 5 points per dollar) than CSR (3X) on restaurant spend. Amex should scrap the "$200" Uber and airline travel credits and focus on MR point rewards for restaurant spend. My Amex Platinum card stays in the drawer at home while the CSR is at the top of my wallet because it's used (almost) every day at a restaurant. CSR's 3X bonus means it gets used every time I eat out (even if it's $10 spend). With the higher merchant fees that Amex charges (versus Visa or MasterCard), Amex should be able to pass along those higher merchant fees to its premium card holders through fat MR bonuses. Not many people travel all the time, but it's fair to say that everyone eats all the time. Furthermore, frequent card usage at restaurants means the card is seen by a maximum number of people (both customers and restaurant staff).

Amex Platinum should [ditch the $200 credits and] give 5X points per dollar spent at restaurants, 4X points per dollar on airline/hotel/travel, 3X points for gas & groceries, and 2X on all other spend. MR bonuses like those would keep the Platinum card in everyone's wallet (or purse) and justify the $550 annual card fee. As it is now, Amex tries to incentivize Plat holders to meet minimum spending thresholds to earn one-time signup or retention bonuses, but gives them little incentive to keep it in their wallet beyond that (initial bonus). Amex needs to stimulate and incentivize general everyday spend by Platinum card holders, instead of focusing only on big-ticket (and less frequent) travel purchases.

450 was borderline but 550 is done.

@The Oracle - I think getting the airline credit is fairly easy, thanks to the ability to buy gift cards. If that avenue was cutoff, then yes it could be difficult using the credit due to the hassle of checking a bag, high cost of buying food / drinks onboard, etc...

Now the Uber credit is another story. The fact that you have to use it once a month is awful and I'll be lucky...

@The Oracle - I think getting the airline credit is fairly easy, thanks to the ability to buy gift cards. If that avenue was cutoff, then yes it could be difficult using the credit due to the hassle of checking a bag, high cost of buying food / drinks onboard, etc...

Now the Uber credit is another story. The fact that you have to use it once a month is awful and I'll be lucky to break even with it. It'll be very interesting next year once annual fees come up and if AMEX will negotiate with some users that didn't use at least half their AMEX credit and complain that it directly affects the annual fee.

I'm beginning to not like my amex platinum card. Their concierge service can't get me into anything I've requested where as citi prestige has been able to. Not only does it feel like they could careless but also seems like they have no clout.

Anyone else have the same issue?

I've only held the business version for the past year. Your analysis is good when deciding whether or not to keep both cards but not good if deciding if one or the other is better. Hilton, SPG, and National status are good. Priority Pass is lagging domestically. Biz card adds 10 gogo full flight passes annually. Centurion Lounge access is poor anymore. Not sure it's worth $250 for the biz card. But if I can...

I've only held the business version for the past year. Your analysis is good when deciding whether or not to keep both cards but not good if deciding if one or the other is better. Hilton, SPG, and National status are good. Priority Pass is lagging domestically. Biz card adds 10 gogo full flight passes annually. Centurion Lounge access is poor anymore. Not sure it's worth $250 for the biz card. But if I can also deduct as @pak says it might get a little better to hold onto it...

At slightly over 1.5 cpp, I would just go with Chase, way less fees, and more ways to earn bonus points. I love Centurion Lounges, but I can't justify that expense. However, if you are a major ANA miles user, that would keep me with Amex. Again though, it still doesn't justify $550/year.

If you are using the card for business then you can deduct the annual fee - depending on your tax bracket the annual out of pocket / breakeven is much lower

I think your math is missing something. The reason Amex couldn't sustain 50% rebate is not because it can't sustain a 2-cent per point value, it is that it can't sustain a 10-cent per dollar value. There are plenty of no-annual-fee cards out there that have 2% cash back but for those cards 2% is the cap. With Amex Plat Biz, if you spend the right way (ie on flights) you were get 10% cash...

I think your math is missing something. The reason Amex couldn't sustain 50% rebate is not because it can't sustain a 2-cent per point value, it is that it can't sustain a 10-cent per dollar value. There are plenty of no-annual-fee cards out there that have 2% cash back but for those cards 2% is the cap. With Amex Plat Biz, if you spend the right way (ie on flights) you were get 10% cash back.

If you continue to think redeeming points via CC travel portals is a good value, AMEX's rebate offer is better than the CSR if you have a lot of airline spend. You get 7.7% back per dollar vs 4.5% back. The math obviously goes down for AMEX if you are not spending in bonus categories either on the Plat or any other MR card.

I got the Amex Plat personal May last year , so on my next statement this year will I get $450 annual fee or $550

I just closed my Mercedes-Benz Platinum (Monday) and now am thinking of going for the Charles Schwab Platinum, which has a higher bonus right now (60K). How is Amex on closing and then applying so quickly, in your experience?

I have to disagree. You selectively omit how difficult it is to get the airline credit and that Uber must be used monthly or it is lost. Additionally, Centurion lounges are crowded 24-7. All this for an extra $100 Annual fee increase. No thanks - I'm cancelling this year when the fee is due.

@Lucky - Don't forget about the Global Entry Credit; for those that don't have it when they apply for the card, the out of pocket then is more like $100.