Yesterday we learned about a new electronics ban for certain flights to the United States. Later in the day the United Kingdom announced a similar (yet very different) policy for flights to the UK.

While I’m not going to get into all the ramifications here, the gist of it is that travelers are going to have to choose between connecting elsewhere or risking damage and theft of their personal electronics (ins).

Reader Mike summed it up nicely:

“My bet is there will be lots of $2,000 insurance claims for Apple laptops forced to endure the cargo experience. Whoever Chase, et al, use for travel insurance is going to get very busy.”

That’s a great point, but it’s much more complicated than that. Not all policies necessarily cover checked electronics, and many have strict dollar limits. So I figured it would help to go through the various options for insuring your gadgets when traveling.

What has to be checked?

If you are flying directly to the United States from the following airports, all electronics (with the exception of cell phones and medical devices) must be checked into the cargo hold:

- Amman, Jordan

- Abu Dhabi, United Arab Emirates

- Cairo, Egypt

- Casablanca, Morocco

- Dubai, United Arab Emirates

- Doha, Qatar

- Istanbul, Turkey

- Jeddah, Saudi Arabia

- Riyadh, Saudi Arabia

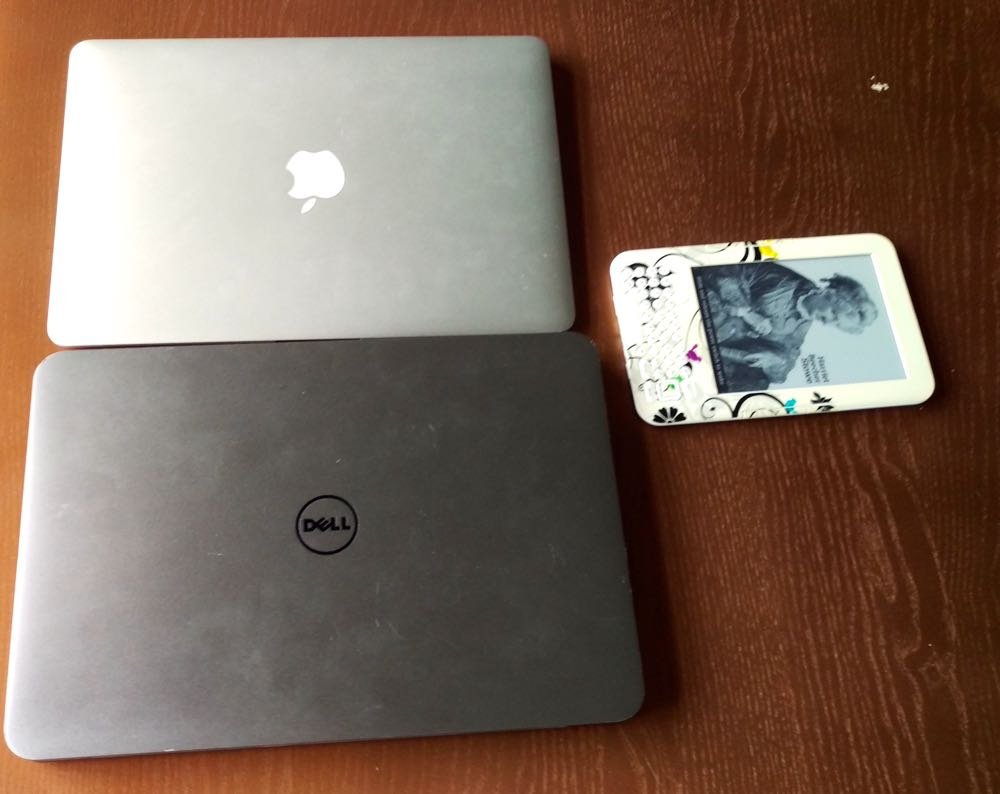

For my husband and I, who actually travel really light in electronics compared to many people (no tablets in our house), that would mean checking all this stuff:

Meanwhile, if flying directly to the United Kingdom from the following countries, all screen-containing devices larger than a cell phone must be checked (cameras and other electronics are not included in the UK ban):

- Egypt

- Jordan

- Lebanon

- Tunisia

- Turkey

- Saudi Arabia

So for us, that would mean checking the following:

And just to hammer home the discrepancy between the two policies, because it boggles my mind that some people can’t recognize the difference, here is what we would have to check if we were flying to the United Kingdom from Qatar or the United Arab Emirates:

Yes, gratuitous puppy photo because sometimes working from home is complicated, and otherwise this would be a picture of an empty table. I don’t recommend trying to import a puppy to the UK though, it’s very complicated.

So, let’s look at the coverage options.

Credit card coverage

Many credit cards offer some kind of travel insurance, including for travel delays and baggage protection. Each card has slightly different rules and exclusions, however, so you’ll want to carefully read the benefits pamphlet that comes with your card.

There are a few things to watch out for:

- Only certain people (such as immediate family) may be covered

- How the ticket is purchased matters (award tickets or those purchased in foreign currency may not be covered)

- Coverage limits may be divided between carry-on and checked baggage

- High value items may not be covered at all, or at a very low limit

- Business cards may only cover proven business trips

Here’s a comparison of the baggage insurance policies of some of our favorite travel rewards cards:

- Earn 5x points on flights purchased directly from airlines or through Amex Travel (up to $500k/year)

- Earn 5x points on prepaid hotels through Amex Travel

- Annual Fee: $695

- Up to a maximum of $2,000 for each Covered Person on a Covered Trip

- Maximum benefit of $250 for loss of high risk items such as jewelry, sporting equipment, photographic or electronic equipment, and computers and audio/visual equipment

Fare is charged to the Basic or Additional Cardmember’s American Express Card and payable in full in U.S. dollars or combined with American Express Membership Rewards® Points. (Does not include award tickets)

- Earn 5x points on flights purchased through Amex Travel

- Earn 5x points on prepaid hotels purchased through Amex Travel

- Annual Fee: $695

- Up to a maximum of $2,000 for each Covered Person on a Covered Trip

- Maximum benefit of $250 for loss of high risk items such as jewelry, sporting equipment, photographic or electronic equipment, and computers and audio/visual equipment

Fare is charged to the Basic or Additional Cardmember’s American Express Card and payable in full in U.S. dollars or combined with American Express Membership Rewards® Points. (Does not include award tickets)

- Earn 3x points on travel

- Annual Fee: $95

- Up to three thousand ($3,000.00) dollars for each Insured Person (you and your Immediate Family Members) for each Common Carrier Covered Trip

- Up to five hundred ($500.00) dollars for jewelry, watches, cameras, video recorders, and other electronic equipment

Some portion of the fare for transportation has been charged to your Account, or when free flights have been awarded from frequent flier or Rewards programs, provided that all of the miles or Rewards points were accumulated from a Rewards program sponsored by Chase Bank USA, N.A. and/or its affiliates.

The clear winners here are the premium Citi cards, and specifically the Citi Prestige® Card. I already charge my international travel and award tickets to the Prestige due to the delay protection, so this is another incentive to do so.

For those who travel with tablets and e-readers, but not laptops, the lower coverage limits on the other cards might be sufficient — it’s just going to depend on your situation.

Separate travel insurance

In theory, travel insurance policies should cover lost or damaged baggage as well. I’m not terribly familiar with the travel insurance market, as in order for award tickets to be covered you typically have to purchase a more expensive policy, and cancelation fees on award tickets are typically so reasonable.

So I did some research.

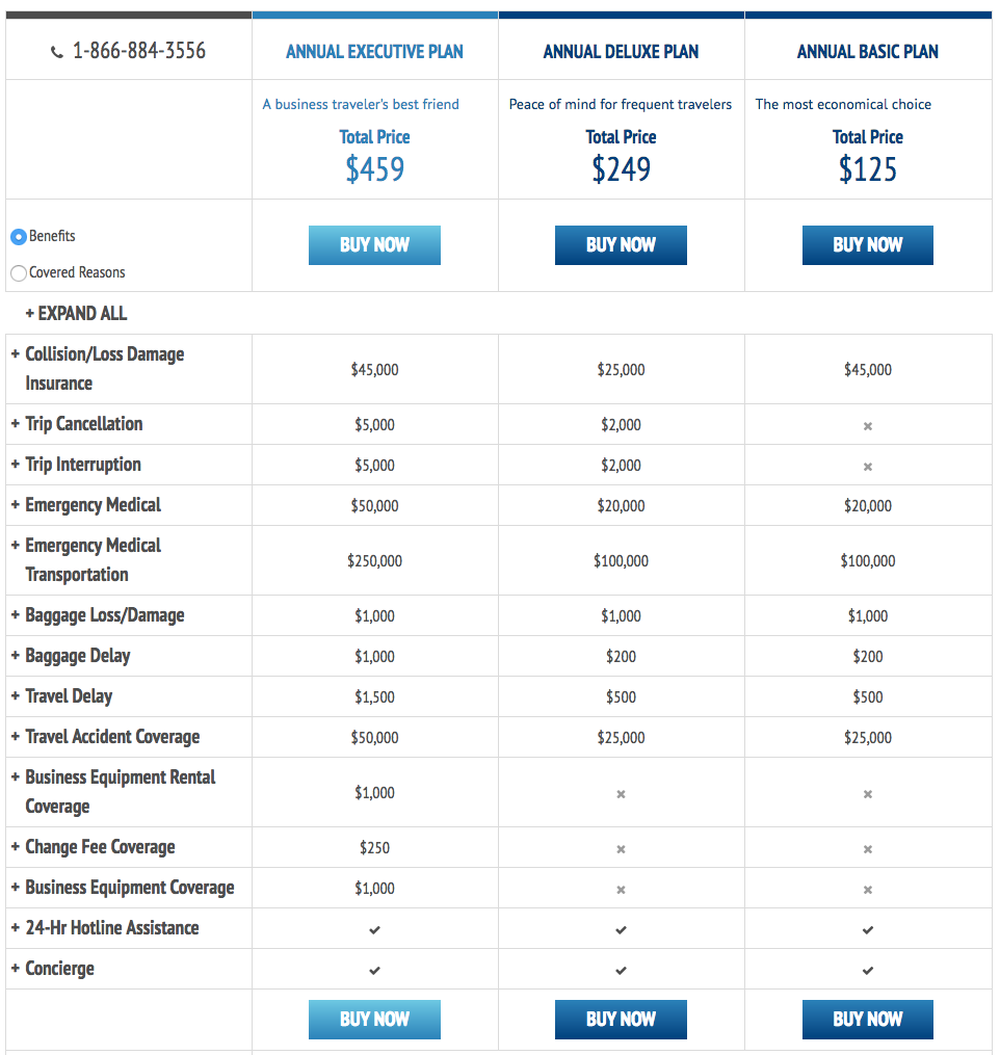

Allianz offers annual policies, which seem like they could be a good option for frequent travelers instead of purchasing individual trip policies (though again, it depends on your travel patterns).

Even if you purchase the more expensive Executive Plan, however, you’re still capped at $500 in total for high-value items.

So while there are other benefits of travel insurance that might be worthwhile, I’m not sure it makes sense to take out a policy in hopes of covering checked electronics.

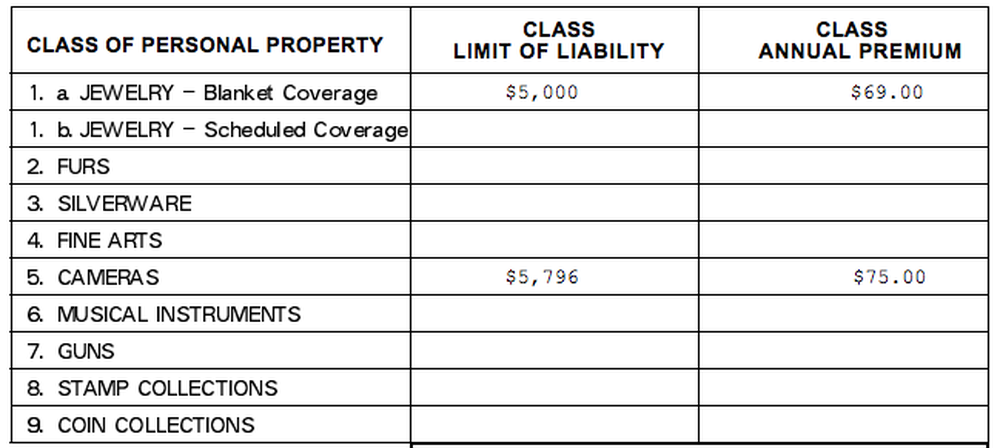

Homeowners/Renters insurance

Another option may be to work with your personal homeowners or renters insurance company. For high-value items, the coverage isn’t necessarily automatic, but you can typically purchase a separate rider ahead of your travel.

This is what we’ve done in the past, as my husband travels with an abundance of expensive camera equipment. We pay $75 a year for full replacement-value coverage of his cameras and lenses:

Of course, many people have an aversion to filing a claim against their property insurance, as there’s a risk of premiums increasing and so forth. But it’s an option, particularly for renters.

You have to prove you own this stuff

Regardless of which insurance coverage you’re counting on, you’re going to have to be able to document your ownership of these items. You can’t just claim that you had an iPad “mysteriously vanish” from your checked luggage.

So before you travel, you’ll want to make sure you have some kind of documentation. This might include receipts, serial numbers, or even photos of the items.

You’ll also need to prove the value of the items. Some policies offer the full replacement value (so even though we purchased a camera lens for $200 on Craigslist, it’s covered for the $1500 it would cost to replace it), others offer a depreciated value based on the age of the item.

Be prepared to document all of this. A shared folder in Google Drive with scans of everything works brilliantly in our house.

You have to prove you lost something

This is the obvious corollary to having to prove ownership, but since we’re being thorough — you will likely have to provide evidence that you are missing something.

In reading through these policies, they all require you to submit a claim with the airline first, and provide evidence of having submitted that claim. There are also deadlines for doing so (some as short as 72 hours!), so be sure to read your policy terms carefully.

As an example, here is the list of documentation of items lost/damaged in checked baggage that Chase notes as being potentially required for their insurance company:

- a completed claim form

- a copy of the travel itinerary

- written confirmation that the claim was filed with the Common Carrier

- a copy of the credit card statement that shows the charge for the Common Carrier fare

- a copy of the settlement or denial from the Common Carrier

- copies of receipts for the purchase of replacement items over twenty-five ($25.00) dollars

- copies of original receipts

So again, being organized will be key. Having all this information scanned and stored in the cloud ahead of time will absolutely make life easier.

Bottom line

Checking electronics or high value items is generally not a good idea — you’re exposing them to theft and risk, and insurance actuaries know that. If this electronics ban becomes a longstanding thing, we might see companies adapt their polices to provide better coverage, but in the meantime most are very limited.

Obviously the best strategy for business travelers will be to avoid routes requiring you to check your electronics, but there’s always a chance of being re-routed. And for leisure travelers, having to check their tablets might not be a deal-breaker, so it’s good to know what and when is covered.

Regardless of which coverage option you choose, you’ll want to be super organized, with thorough documentation in order to file a claim.

Have you used baggage insurance? What was your experience?

Wow, I'm always amazed at the amount of paperwork that's needed to claim for stolen electroncis. I suppose that keeping claims difficult cuts down on fraud, and keeps costs down, but it's such a hassle for those with genuine claims.

Great article, btw! And loved the gratuitous puppy photo. Keep 'em coming.

Agree with @Miz. Citi's insurance sounds good, but if they (Virginia Surety) don't pay valid claims, it's worthless.

Though far from perfect, Chase and Amex do much better when it's covered. I've more or less stopped using my Citi cards because of bad experiences with valid claims.

I think what gets lost in this entire discussion is the potential for lost productivity at your destination. Even presuming your business (or you personally) are willing to check electronics - what happens if you are rerouted due to weather or a mechanical and your bag doesn't make it? Or makes it 48 hrs later? Yes, you may get your electronics back, but you just lost two days of work.

Tiffany: Thank you for this very well written article!

Also, more pictures of your dog!!

Regarding a camera lens, while I agree that it should not be part of the ban, does anyone really thinks the security trolls are going make that distinction? They are mindless and will see "camera" and ban it.

The most idiotic part about that is in my opionion the fact that you will be allowed to take everything with you when you fly DXB-MXP, MXP-JFK.

Isn`t this new rule just ridicoulous?

I am a Virtuoso travel specialist and travel writer and a year ago my husband inadvertently packed his ipad and go pro and several cords from other cameras and computers, chargers etc.. Every smidgen of cords and all electronics, camera equipment (cases/accessories for go pro) were all gone from the suitcase. We had three different insurances and none of them would even pay for a cord! Then and until now, airlines categorically refuse to compensate...

I am a Virtuoso travel specialist and travel writer and a year ago my husband inadvertently packed his ipad and go pro and several cords from other cameras and computers, chargers etc.. Every smidgen of cords and all electronics, camera equipment (cases/accessories for go pro) were all gone from the suitcase. We had three different insurances and none of them would even pay for a cord! Then and until now, airlines categorically refuse to compensate for anything at all under those categories. It will be very hard to enforce that if you have no choice but to check those items.

The baggage handlers and delivery people (they conveniently refused to let us pick up our luggage in transit saying we were on Canadian passports and were not allowed because they could not put us as through connections, even though we were on a star alliance tickets.

I think the airlines should be pressed for a statement to clarify the policy and as others have said, perhaps it will become another separate rider to pay for, or include to a certain low level, which is still better than none, because it means that the handlers will have to be accountable.

.

Won't the primary insurance be from the airline? If so how much will it cover?

@Tiffany: Looking at your first picture I believe you don't need to check the lenses which are usually the most expensive part of the camera. The body is electronic but as you said it should be covered by homeowner's insurance. You can always buy a cheap laptop just for browsing and using MS Office and keep all your files in a high capacity pen drive (which you can carry with you) or in the cloud....

@Tiffany: Looking at your first picture I believe you don't need to check the lenses which are usually the most expensive part of the camera. The body is electronic but as you said it should be covered by homeowner's insurance. You can always buy a cheap laptop just for browsing and using MS Office and keep all your files in a high capacity pen drive (which you can carry with you) or in the cloud. I think this electronic ban is a huge inconvenience but for travelers like you and other bloggers I don't think it is such a huge deal that you cannot find ways to solve it without extra insurance.

@ Santastico -- It's a creative solution, but I already keep all my files secured in the cloud. My hard drive has very little data (mostly just resized pictures and such), because I am generally concerned about data protection with all the traveling I do, so that's not my concern as much. Still, I will avoid these routes.

It means checking a bag, which ruins my flexibility in case of IRROPS, and otherwise hurts...

@ Santastico -- It's a creative solution, but I already keep all my files secured in the cloud. My hard drive has very little data (mostly just resized pictures and such), because I am generally concerned about data protection with all the traveling I do, so that's not my concern as much. Still, I will avoid these routes.

It means checking a bag, which ruins my flexibility in case of IRROPS, and otherwise hurts my productivity. Checking a bag means arriving at the airport earlier, and leaving later. It means either risking that I won't have key items at my destination, or having both a cabin bag and and checked bag.

It's not just the fear of lost equipment, but also the threat of lost time. There's the time on the flight (I typically work or sleep on a flight -- I'll watch maybe two movies a year on planes), which is significant. There's also the time in the lounge, the time between boarding and departure (I can get a solid 45 minutes of work done while everyone else is boarding, more if there's a delay), the extra time spent waiting for a bag on arrival...It all adds up to be quite significant, and I'm sure I'm not the only one facing similar constraints.

@fred:

No, but I can do math, and I can read. Fortunately the FAA publishes guidelines that allow others with these abilities to make informed decisions.

However, you are confused as to the meaning of "spares". What the FAA asserts as a spare battery (again by the linked document) is one that lacks internal power protection. Batteries of this nature are those that are installed in another device (camera batteries, also phone and laptop batteries...

@fred:

No, but I can do math, and I can read. Fortunately the FAA publishes guidelines that allow others with these abilities to make informed decisions.

However, you are confused as to the meaning of "spares". What the FAA asserts as a spare battery (again by the linked document) is one that lacks internal power protection. Batteries of this nature are those that are installed in another device (camera batteries, also phone and laptop batteries before they were non-removable). A portable battery pack intended for charging USB devices contains internal protection circuitry for overvoltage, overcurrent, and other failure situations (electrical shorts, etc). Since it has these protections, it doesn't meet the requirements that the FAA requires to be considered a spare battery.

TL;DR: checking your USB power bank is no different than checking your MacBook.

@hubs

Being an electrical engineer does not make you a reliable source on knowing what batteries are allowed to be carried on airplanes. Also, on the document, it says you cannot bring lithium ion spares in your checked baggage.

@Nick W: USB power banks are absolutely allowed, even as stated by the document you linked to.

The largest of these typically run around 20000mAh, or 100 watt-hours. Per that link, each traveller may carry up to two batteries of this size. And remember, all power protection circuitry is contained within the device; the category of "unprotected" batteries only applies to removable batteries not installed in a device, such as removable camera batteries.

Source: I'm...

@Nick W: USB power banks are absolutely allowed, even as stated by the document you linked to.

The largest of these typically run around 20000mAh, or 100 watt-hours. Per that link, each traveller may carry up to two batteries of this size. And remember, all power protection circuitry is contained within the device; the category of "unprotected" batteries only applies to removable batteries not installed in a device, such as removable camera batteries.

Source: I'm an electrical engineer.

As someone who is going to be facing this exact situation next week (return trip on connecting flight going through dxb) I noticed emirates at least hasn't sent any email notices yet to booked travellers about the new mandate. Also still waiting to hear what corporate will issue as guidance with regards to the laptops in checked baggage as that will likely need a separate insurance rider being mandated on any flights booked for work that go through these airports.

Tiffany you're the best. Please post more often!

Tiffany, I love your posts. That is all.

On the assumption that the Anker device in the first photo is a USB power-bank, you can neither take that into the cabin nor check it: the FAA does not permit external battery packs in checked baggage.

https://www.faa.gov/about/office_org/headquarters_offices/ash/ash_programs/hazmat/passenger_info/media/Airline_passengers_and_batteries.pdf

Insurance is definitely one way to go. Another is for airlines to offer Business travelers built in computers which they can log on to using secured VPN tunnels. The airlines already have wifi and built in TV and sound. Adding computers would give the airlines a real competitive advantage over others where First class and Business travelers are the cream!

Egrace, the policy you're referrrnig to restricts the shipping of lithium batteries as CARGO, not in checked baggage. While airlines in the past have discouraged electronics from being checked, that's largely because they couldn't guarantee that they wouldn't be damaged or stolen. There's never been a blanket policy against checking individual electronic items containing lithium batteries,

American Express used to offer, not sure if they still offer it to new enrollees, an extra travel insurance with their Platinum that you could enroll in and pay $24 per ticket and be you'd covered on award tickets as well. I'm not sure of the amounts on the top of my head but I can check my file when I get home. If I remember right it was well above any other cards offerings....

American Express used to offer, not sure if they still offer it to new enrollees, an extra travel insurance with their Platinum that you could enroll in and pay $24 per ticket and be you'd covered on award tickets as well. I'm not sure of the amounts on the top of my head but I can check my file when I get home. If I remember right it was well above any other cards offerings.

They also used to offer a travel medical insurance you would use for primary insurance when traveling and it is only $13 a month for a family of 4.

I've used both of these insurances before and they are excellent.

Also, how would this policy apply on flights like Dubai-Milan-JFK and Dubai-Athens-EWR?

I'm wondering whether the credit card companies will begin to change their insurance policies etc as well given the changes.

One other options I wonder if airlines/TSA could consider is along the lines of what they do for duty free purchases: namely, they are given to you in a sealed bag. What if when you went through security, laptops and cameras had to be inspected and then put in sealed bags that you were...

I'm wondering whether the credit card companies will begin to change their insurance policies etc as well given the changes.

One other options I wonder if airlines/TSA could consider is along the lines of what they do for duty free purchases: namely, they are given to you in a sealed bag. What if when you went through security, laptops and cameras had to be inspected and then put in sealed bags that you were not allowed to open upon landing?

The biggest worry (to me) of checking in laptops and the like is not theft, but damage. Checked baggage is jostled around pretty intensely.

@Tiffany I don't think you have to check the lens as that is not an electronic device.

The one thing that jumps out at me with this new policy is that is directly conflicts with the airlines policy of No lithium batteries in the cargo hold. So wtf are we supposed to do?

I was doing my 1st lost baggage claim (i.e damaged checked bags) and I put my spend on the the Chase united Mileage Plus card. In the list you have provided, you missed out that card.

All the benefits what you have noted there for other chase cards are pretty close and applicable to Mileageplus card.

Now here in my pain regarding the claim. The insurance folks are asking "a copy of the settlement...

I was doing my 1st lost baggage claim (i.e damaged checked bags) and I put my spend on the the Chase united Mileage Plus card. In the list you have provided, you missed out that card.

All the benefits what you have noted there for other chase cards are pretty close and applicable to Mileageplus card.

Now here in my pain regarding the claim. The insurance folks are asking "a copy of the settlement or denial from the Common Carrier". My flight involved 2 carriers United and Air India.

My 1 checked bag was hopelessly ripped off on all side and teriibly broken on all sides to such an extent that they had to plastic wrap it entirely. A bag damage report was filed at Newark.

Now the worst part is, that damm airline doesn't respond to any of my emails since the last 1 month.

And the CS have no clue as they always direct me to Airport staff.

I have now contacted United for help and got to see what is going to happen.

All I need is a letter from the airline saying where they settle or deny my claim which is what required for the insurance folks.

Does Chase Ink Plus Business not provide any benefits? I noticed the chart mention Ink Preferred but not Ink Plus

@ toucan -- It should, but the card is no longer available to new applicants, so I couldn't verify the benefits terms.

Citi insurance is provided by Virginia Surety which lacks surety. Although sometimes they approve the claims, they have a strong tendency to use all sorts of non-sense excuses to deny the simplest of claims.

I won't say Citi's insurance is a winner under any circumstance.

Great post Tiffany !! Something similar for medical coverage/repatriation beyond Allianz options would be welcomed!

like most insurance, it all sounds good until you put in a claim ?

The value of the item is not the worry- the information in the laptop -i-pad etc that is the real cost - many keep banking info etc on the device - better get everything encrypted

Nice information about what's covered and what's not. I wonder how often electronics get stolen from checked luggage. I normally do not check anything in unless I have to. I also wonder whether we'll start seeing US-bound flights from the Middle East area targeted for electronics theft because the thieves will know there's a high chance of catching loot or whether the airlines will come up with a way to deter would-be thieves and allay...

Nice information about what's covered and what's not. I wonder how often electronics get stolen from checked luggage. I normally do not check anything in unless I have to. I also wonder whether we'll start seeing US-bound flights from the Middle East area targeted for electronics theft because the thieves will know there's a high chance of catching loot or whether the airlines will come up with a way to deter would-be thieves and allay travelers' fears.

At any rate, this ban is supposed to last until mid-October. My guess is that it either gets expanded to cover all flights or gets dropped by that date.

I have a nagging suspicion that the travel insurance companies will come up with a product or rider on top of their plan to cover high end electronics beyond the typical $500 minimum. That way they can reach a whole level of new customers or increase their revenue on existing ones.