If you’ve ever traveled abroad and paid for something by credit card, you’ve almost certainly been asked “would you like to pay in [local currency] or [your home currency]? For example, if you’re in Europe and using a credit card issued in the United States, you’ll probably be asked if you want to pay in US Dollars or Euro.

The short answer is that you should just about always pay in local currency, yet it amazes me how often I observe people not doing that. I’m sure savvy travelers know the right answer, though in this post I wanted to take a closer look at the topic of dynamic currency conversion.

In this post:

What is dynamic currency conversion (DCC)?

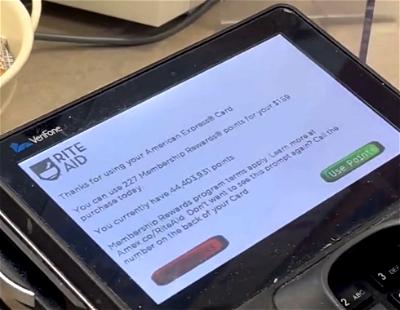

Dynamic currency conversion is essentially a “service” provided by credit cards and payment networks that gives card members the option of paying in their billing currency rather than the local currency. In other words, if you’re in Europe, you’ll likely be billed in Euro, even though that may not be the currency in which your credit card bills you.

The same principle applies at ATMs. If you’re trying to withdraw Euro, you’ll be asked whether you want to just withdraw that number of Euro at the standard exchange rate, or whether you want that amount converted on the spot, so that you know exactly how many US Dollars your account will be debited.

What are the benefits of dynamic currency conversion, whereby your purchase will be converted to your billing currency on the spot? Well, it guarantees the amount that you’ll pay in your billing currency, regardless of any exchange rate fluctuations. Furthermore, it provides transparency as to how much you’ll pay in your billing currency, especially if you’re not great at math and/or don’t know the exact exchange rate.

When some people are asked whether they want to pay in their home currency or the local currency, they might think “oh, how nice that they’re willing to convert it, that’s convenient.” However, there’s a major catch.

Should you use dynamic currency conversion?

Please, please, please, don’t use dynamic currency conversion, because it’s almost never a good deal. I don’t want to go so far as to say it’s a scam, because there’s generally quite a bit of transparency around it, and you’re just being given two options. However, it’s kind of like asking someone “hey, do you want to buy a $100 gift card for $110?” Um, no, why would anyone want to do that?

Let me give an ATM example. I’m in Italy at the moment, and tried to withdraw 200 Euro from an ATM. I was given the option of withdrawing the amount in my home currency, US Dollars

No matter how I choose to do the transaction, there’s a €3.95 transaction fee, which is standard (though many banks reimburse this). I was then given the option of having that amount debited from my account (in Euro) at the standard exchange rate, or I could instead be debited $254.88, including a 12.95% markup. That’s right, the dynamic currency conversion fee here is 12.95%.

Of course I declined that, so I ended up paying $225.67 for the €200, and then Chase reimbursed me the $4.37 terminal fee in a separate transaction.

So the question literally comes down to whether you’d rather pay $254.89 or $225.67 (before the fee reimbursement, in my case) for 200 Euro. I know which I’d pick. 😉

If you’re using credit cards, the dynamic currency conversion fee typically isn’t quite as much. It varies depending on the payment processor, merchant, etc, but is more likely to be in the range of 1-5%.

Why does dynamic current conversion even exist?

If dynamic currency conversion is almost universally a bad deal, why is it even offered? Well, I think the answer is pretty obvious. Take the above ATM example, where there’s a 12.95% markup. I am sure a not insignificant number of people select that option, so there’s more money to be made this way.

That money primarily goes to financial service providers who market the dynamic currency conversion system, but also to merchants and ATM operators, who receive a commission on each transaction carried out via dynamic currency conversion.

Now, fortunately a vast majority of merchants are pretty ethical, and will just give you the option of which you want (as they’re supposed to). However, every once in a while you might run into a merchant who either by default charges you in your home currency using dynamic currency conversion, or who claims it’s a better deal. That’s highly unethical, of course.

How do credit card foreign transaction fees fit into all of this?

If you travel abroad you absolutely should have a credit card with no foreign transaction fees. You don’t need to be a high roller to get one of these cards — there are even lots of great no annual fee cards that don’t have foreign transaction fees.

If you use a no foreign transaction fee credit card abroad, just decline dynamic currency conversion (meaning you should pay in local currency), and you should get your purchase converted at a pretty fair exchange rate.

What happens if you use a credit card that does have foreign transaction fees? These fees are typically somewhere around 3%. Foreign transaction fees are normally based on the currency in which you make a purchase, rather than the country in which you make a purchase.

In other words, accepting dynamic currency conversion at the point of sale would potentially allow you to avoid these fees. However, the fees associated with dynamic currency conversion are often more than 3%.

Really the moral of the story is that you should have a card with no foreign transaction fees, as you’re otherwise going to lose a few percent on each transaction, potentially, and that quickly adds up.

Bottom line

Dynamic currency conversion is something that you’ll constantly deal with when making purchases in a foreign country. Your takeaway should be that you should always choose to be charged in the local currency rather than your home currency, regardless of whether you’re making a credit card transaction or withdrawing money from an ATM. Furthermore, make sure you have a credit card with no foreign transaction fees.

It amazes me how often I see well traveled people use dynamic currency conversion, despite paying with a card that has no foreign transaction fees. Don’t make that mistake.

See my post on how to exchange foreign currency efficiently.

Is anyone else surprised by just how many people seem to use dynamic currency conversion?

"Always Choose Local Currency"

But, for those who have a card issued outside the United States or the Euro Zone, you should always choose US Dollar.

Not really, actually no.

"Always Choose Local Currency" still applies.

@Eskimo, I agree, why would you choose a poor exchange rate to the USD rather than your bank's rate to your own currency. That's before even considering the absurd implication that a traveller should choose the USD rather than choose the the local currency if their card is issued to be billed in the CHF, GBP, DKR, CAD, JPY, SGD, AUD or NZD or any other freely convertible currency. I chose the USD on my...

@Eskimo, I agree, why would you choose a poor exchange rate to the USD rather than your bank's rate to your own currency. That's before even considering the absurd implication that a traveller should choose the USD rather than choose the the local currency if their card is issued to be billed in the CHF, GBP, DKR, CAD, JPY, SGD, AUD or NZD or any other freely convertible currency. I chose the USD on my most recent trip, but that was because it was the local currency, and I knew my card's conversion rate was far better than the one the merchant offered.

There is one caveat. I would prefer to pay for credit card holds (like in hotels and car rentals) in home currency. Reason: It comes back.

I had an interesting experience with paying for hold with GBP in 2016. 500 pounds was on hold and it came back in 6 days. However, if you recollect events in 2016 in the UK, the value of the pound was close to 8% down in those 6...

There is one caveat. I would prefer to pay for credit card holds (like in hotels and car rentals) in home currency. Reason: It comes back.

I had an interesting experience with paying for hold with GBP in 2016. 500 pounds was on hold and it came back in 6 days. However, if you recollect events in 2016 in the UK, the value of the pound was close to 8% down in those 6 days! I lost $56!! Usually they don't let you split the hold and the payment, but if they do, I'd put the hold in home currency.

Your experience works both way.

If GBP was up 8% you would have made $56.

No one could have predicted the forex market. But if you could, you'd be making crazy money to even care about $56.

I buy my Australian dollars at my local Chase bank before leaving the USA. Forget the airport exchange booths and ATM's! Buy your Aussie dollars or Euros in the USA and travel with the hard currency in a secure carrier. Just be careful!

In New Zealand they must have cracked down on this because atms have a very good conversion rate (from what I saw a few times this year).

There have been plenty of times I have clearly declined DCC, but when the restaurant runs the final transaction, they do not honor the selection. I always keep my receipts (showing where I declined DCC), and dispute the charges. Chase makes it really easy, where you can select the dispute reason as "charged in wrong currency." One reason merchants like to do this is that the interchange fees are reduced when the customer selects DCC...

There have been plenty of times I have clearly declined DCC, but when the restaurant runs the final transaction, they do not honor the selection. I always keep my receipts (showing where I declined DCC), and dispute the charges. Chase makes it really easy, where you can select the dispute reason as "charged in wrong currency." One reason merchants like to do this is that the interchange fees are reduced when the customer selects DCC -- so I very much want the merchant hit with dispute fees to discourage the practice. One time, I had a hotel insist on being paid in USD. I suggested we call the police, because I was in Korea and therefore was only willing to settle my bill in KRW. The manager quietly changed the currency and swiped my card.

Well, I think it depends where you are going. Some currencies have a huge amount of inflation whereby choosing USD is the best option. Furthermore, sometimes you are not given a choice as to which currency to use. Also, it is not as plainly presented as it is on the ATM. You can see the comparison of the Dollar figures, but with a credit card transaction usually you cannot.

If the foreign currency inflates, then USD becomes even worse, not better. Merchant agreements with cardholders require them to let you choose the currency. Naturally merchants may violate this in practice. If you find yourself forced into DCC, sign the receipt with "DCC refused," then inform your credit card company.

*card issuers, not cardholders

Currencies getting 6% stronger against your own in the ?2 days between charge, and it hitting your statement, are pretty rare!

If you did know that was coming, take out an option for a big notional and then retire!

I mean, really depends on circumstances. I used to have a bank account which charged a few pounds per transaction in a different currency plus a percentage. Therefore, it was far better to take the bad exchange rate on small purchases.

These days it is much easier to have a bank account with no transaction fees, but there are still things to watch out for.

For instance, your blog often talks about the...

I mean, really depends on circumstances. I used to have a bank account which charged a few pounds per transaction in a different currency plus a percentage. Therefore, it was far better to take the bad exchange rate on small purchases.

These days it is much easier to have a bank account with no transaction fees, but there are still things to watch out for.

For instance, your blog often talks about the different AmEx credit cards, but if you live outside of the US, AmEx cards are rubbish for foreign transactions. Whenever you make a transaction that is not in your home currency, they convert it to USD and then convert it to the other currency. Plus they charge the 2,99% fee.

If you are not American then a lot of travel advice differs. Your non-US AMEX has all sorts of differences. Based on what you're saying here though it seems DCC is still a bad choice because the DCC markups I have seen were all significantly above 2.99%.

@Grey makes two good points:

1) About fixed fees as well as percentage, which is material for small amounts.

Still true for cards issued in less competitive/developed markets.

2) Amex can be a 1% spread twice, plus the 3%.

Still less than DCC 7%.

Mastercard (but not Visa) in non-EUR EU countries converts first to EUR and then on to the local currency.

When I go to a foreign country, I always find a reliable and honest moneychanger to get a wad of cash in the local currency. I avoid airport moneychangers (except for a token $100 USD exchange if I have absolutely zero local currency in cash) because they typically give you a horrible exchange rate. When using a credit card, I always go for the US dollar choice. My US banks always give me a good...

When I go to a foreign country, I always find a reliable and honest moneychanger to get a wad of cash in the local currency. I avoid airport moneychangers (except for a token $100 USD exchange if I have absolutely zero local currency in cash) because they typically give you a horrible exchange rate. When using a credit card, I always go for the US dollar choice. My US banks always give me a good exchange rate. If you choose the local currency as payment, the local banks and others involved in the transaction ALWAYS pile on excess fees and other costs. My advice: NEVER chose to convert to the local currency at your point of purchase in a foreign country. You'll lose every time.

Your advice is the complete opposite of this post. I think you have gotten it backwards.

With cash, you should never be changing currencies if you can avoid it. Use your home bank's ATM card to get local cash from a local bank's ATM.

This post is either written by an extremely confused person or a clever troll.

I don't normally advocate for censorship but this comment is harmful and should be deleted.

There are a lot of noobs out there that take this conversion specifically because the ATM shows the user their "home currency" which elicits a level of comfort and familiarity. If you don't understand fx rates and basic finance you will select the USD option in Italy more times than not. These machines make an absolute fortune off others lack of financial knowledge.

FX fees for credit and debit cards used to be more than 3% (and in less developed markets) still are.

So there was comment about outrageous overcharging.

When DCC first came in, I assumed that the merchant banks were looking to exploit that overcharging by competitively under-cutting it!

Then I looked at the numbers and saw about 7%.

Some users may assume without checking that the alternative to a high charge...

FX fees for credit and debit cards used to be more than 3% (and in less developed markets) still are.

So there was comment about outrageous overcharging.

When DCC first came in, I assumed that the merchant banks were looking to exploit that overcharging by competitively under-cutting it!

Then I looked at the numbers and saw about 7%.

Some users may assume without checking that the alternative to a high charge is a lower charge, rather than a yet higher charge.

Somewhat similar: hotels charge outrageous mark-ups on 'phone calls, so it really is nearly always cheaper to use your mobile even though the roaming rates may seem expensive.

And since you're lecturing about DCC and how bad it is.

PSA: Don't get money from those tiny non bank ATM in convenience store. Not applicable for most readers here but still a sad state of our financial literacy.

I've seen a slip withdrawing $10 just to get hit with $4.50 fee and possibly another $3 out of network from your bank.

The worse is seeing a $10 withdraw denied NSF, which possibly some...

And since you're lecturing about DCC and how bad it is.

PSA: Don't get money from those tiny non bank ATM in convenience store. Not applicable for most readers here but still a sad state of our financial literacy.

I've seen a slip withdrawing $10 just to get hit with $4.50 fee and possibly another $3 out of network from your bank.

The worse is seeing a $10 withdraw denied NSF, which possibly some banks would charge a $15+ NSF fee for that too.

By the way, why are we still using cash?

My bank reimburses those fees, so I basically don't care what they are. Better to find a good bank for travel then to be selective about choosing ATMs.

It's clearly a scam.

They don't disclose the markup at the time, that's what makes it a scam.

I guess it was disclosed on Ben's screen, but rarely at a retail outlet.

Another thing that is important to add is that many card companies will charge the forex fee even if you opt for DCC. I think there is no reason to use DCC, ever. The cashier at the emigration museum in Dublin event made a point of telling me, unsolicited, not to choose it when it came up on the machine

Especially in China watch out for the automatic default to DCC. I’ve had quite a few arguments at hotels and restaurants insisting this was the only option for a foreign card. Obvious BS and I’ve had to refuse to sign the card receipt, tearing it up in one instance. Surprisingly then the manager was able to do the local currency charge!

Not just China, but just randomly everywhere. It's more of not having any idea of what DCC is or training on that part. DCC becomes an extra step that most people have no clue what it and just keep pressing next, which the genius banks default to DCC.

Banks make money off DCC not the establishment.

Partially true. However, as per Mike's example and my experience, it's not due to "more not having any idea/training". Yes, of course that can occur, but merchants deliberately, without thought, selecting DCC on the customer's behalf without mention, and then arguing/refusing to cancel when the customer notices is wilful and due to an intent to increase revenue to the merchant.

As Ben said, the benefits are shared.

Bangkok a few years ago was particularly bad at this - the machine in bars and restaurant was typically presented after the staff had themselves pressed the button to select DCC.

Even though I was using Revolut/Transferwise which are multi-currency per se.

Unfortunately even those cards have a home location which the systems can obtain, and so choose a currency for DCC.

@Ben,

What Chase debit card were you using that waives foreign ATM fees?

Pretty much all the larger banks (and some of the regionals) have products that will refund certain, or all, garbage fees - ATM fees, foreign transaction fees, etc. Typically they target those willing to pay a monthly fee (e.g., what CitiGold used to do), or those considered high net worth (e.g., keep a minimum balance of $200,000, or $500,000, or $1,000,000+ in a checking, savings, retirement, whatever account based on the bank and the amount...

Pretty much all the larger banks (and some of the regionals) have products that will refund certain, or all, garbage fees - ATM fees, foreign transaction fees, etc. Typically they target those willing to pay a monthly fee (e.g., what CitiGold used to do), or those considered high net worth (e.g., keep a minimum balance of $200,000, or $500,000, or $1,000,000+ in a checking, savings, retirement, whatever account based on the bank and the amount they require) and the product is complimentary.

SoFi used to do it for checking accounts with no minimum, though they've since limited it to one network, so basically you pay the fees now.

Chase Private Client and CitiGold and Citi Private Client all offer this.

Schwab Bank offers unlimited fee reimbursement without minimum balance requirement. I would never use a regular bank’s debit card elsewhere.

There are also quite a few credit unions in the US that allow normal people with neither large balances nor high monthly fees to benefit from "out of network" fee refunds. I use Alliant Credit Union, but this is really common for smaller institutions or online-only banks that simply don't have huge networks of ATMs. Obviously, I cannot speak for what may be available outside the US.

Probably some sort of Chase private banking for rich people like Ben (he deserves it though!)

The best card for normal people is the Fidelity Cash Management account. It reimburses ATM fees everywhere in the US and abroad and there are no limits.

A few years ago the DCC caused a lot of hassle for me at the car rental with Hertz in Sicily. I always decline the currency conversion. However in this case I was never ask and the agent who processed my car return and gave me a receipt claimed he can do nothing about it.

I was finally able to get it corrected by Hertz corporate in the US after several back and forth emails and got a refund on their conversion fee.

I had a brief argument about this with a guesthouse proprietor in Switzerland. She insisted that of course it was proper and convenient for me to pay in U.S. dollars. I'm not sure she even understood what I was saying when I expressed doubt that I'd get a fair exchange rate that way. A lot of people assume there's only one exchange rate at any given time. If people better educated themselves, then those airport currency exchange booths would be out of businees.

The only reason airport currency exchange booths are in business is because we still use "paper" money.

You hardly ever see airport travel agent boots is because we hardly use "paper" tickets anymore.

It's very possible to travel around major cities in Western Europe and North America without paper currency.

Visa is the single largest FX user by volume in the world and as such gets the best rates with lower spreds.

Yet I "generally" get 'slightly' better rates with MasterCard.

I have no idea how other Americans manage their card transactions in Italy but from decades of experience, I never opt for dollars for the reasons you state, I only use ATMs associated with banks to avoid excess fees, and I withdraw any needed cash at a singular transaction. And most importantly I make maximum use of credit cards avoiding cash transactions.

This is the way to go.

Not sure why you needed to write anything else other than the headline ;-)

Google SEO indexing likes to see a good chunk of text along with the headline, silly.

.80 (what your screen grab showed) is a horrible rate.

@ RetiredATLATC -- As you'll see written immediately below that, this includes the 12.95% markup. By declining that, I got a much more standard rate.

Hi Ben - your screenshot of the ATM shows similar (if not identical) of what I was faced with last week in FCO airside. However, when I declined the conversion, the ATM just spit my card back out and displayed ‘transaction cancelled’. Tried twice with same results. Once I exited to the baggage claim area, the same bank’s ATM (forgot the bank name) allowed me to decline the conversion and proceed in Euro. May be a fluke…. or by design :(

You explain the conversion game well. Another scam--er option that appears on ATM's is the bank informing via a screen that they propose a conversion rate that is significantly less than the bank rate on your cash withdrawal. I suggest a "cancel transaction" button in response and find another bank's ATM. However, my experience is that this practice is spreading--rapidly.

I'm going to take the opposite position here. In Africa, a vast majority of cards issued for foreign travel are Visa Debit cash passports denominated in USD/EUR which charge a ridiculously high conversion fee for transactions in any other currencies (as much as 30-40% all-in) in addition to per transaction fees (sometimes as high as $7 per swipe in foreign currency). In situations like that, you always want to seek out merchants that offer DCC...

I'm going to take the opposite position here. In Africa, a vast majority of cards issued for foreign travel are Visa Debit cash passports denominated in USD/EUR which charge a ridiculously high conversion fee for transactions in any other currencies (as much as 30-40% all-in) in addition to per transaction fees (sometimes as high as $7 per swipe in foreign currency). In situations like that, you always want to seek out merchants that offer DCC and transact in the card currency to minimize your losses. I'd take 12.95% any day over the 30%+ I'd otherwise be charged.

Bottom line - understand the charges that your specific card levies and work within those, not random "always use DCC" advice from the internet.

So your bank somewhere in Africa recognizes the DCC and doesn't charge you that fee on top. I can only speak from my experience of having European and US bank accounts and DCC in Europe, not all European countries have the Euro after all, is that it's an annoyance that if not careful can cost you a lot of money. Also, I've seen restaurants in the past make the DCC choice for me where I...

So your bank somewhere in Africa recognizes the DCC and doesn't charge you that fee on top. I can only speak from my experience of having European and US bank accounts and DCC in Europe, not all European countries have the Euro after all, is that it's an annoyance that if not careful can cost you a lot of money. Also, I've seen restaurants in the past make the DCC choice for me where I refused to sign the statement and forced them to call the hotline to reverse that charge. This has become less of an issue thanks restaurants being used to people needing to take the terminal in their hands to enter a PIN which gives you time to decline the DCC if no PIN is needed.

While I always appreciate your insight especially with respect to African aviation, you do understand that the target audience of this blog is American!! Hence, somethings are needless to say. I have an African passport and whenever this blog or other related blogs makes comments about visa free, visa on arrival, it's needless to comment that this doesn't apply to Nigerian passport. I imagine that for the majority of American card holders, the above applies

Products designed specifically for travel are always going to try and get you to pay more through markups and additional charges. I've had colleagues from multiple African countries (Kenya, Ghana, Nigeria, S Africa, etc...) pay using a regular credit card in Europe and get a reasonable exchange rate.

I've traveled extensively across Africa with my EUR denominated credit cards and also receive reasonable exchange rates and always decline DCC. I've even had to fight for...

Products designed specifically for travel are always going to try and get you to pay more through markups and additional charges. I've had colleagues from multiple African countries (Kenya, Ghana, Nigeria, S Africa, etc...) pay using a regular credit card in Europe and get a reasonable exchange rate.

I've traveled extensively across Africa with my EUR denominated credit cards and also receive reasonable exchange rates and always decline DCC. I've even had to fight for it a few times when the hotel would insist on charging me in Euros.

But of course, make sure you understand how your specific card / bank deals with it.

@Frog - every country differs. For example in Malawi where I am right now, the VISA exchange rate on credit card transactions is approx. MWK 1050/$ while the exchange rate for cash is MWK 1500/$ officially and over MWK 1600/$ on the black market. It makes very little sense to use your credit card if you have cash available to exchange as a result.

Somewhat surprisingly, legacy airlines often use something pretty close to mid-market rate if one buys a ticket online and selects a different currency.

LCCs add a spread, but nothing like the 7% which in my experience is the typical DCC amount.

@Bagoly - legacy airlines selling through BSP use IATA CCS rates (effectively a clearing house for currency hedging) so there is no benefit to not using midmarket rate. LCCs outside of BSP are free to set their own rates.

Americans frequently don't bother to do the math and banks know this.

Does Airbnb still scam customers by forcing them into DCC?

Airbnb does NOT force you into DCC. There is always an option, at booking, to choose the currency used. Use your home rate for comparisons if you must but then change the price to the local currency. You have to do this at booking because airbnb charges you the full amount when you book, not when you leave

This is false. Airbnb absolutely forces you to pay in your card's currency at a roughly 3% markup. The only way around it is using a card issued in the local country. If you see an option to view rates in other currencies, that is for display only, and you will be charged the inflated home country currency rate at checkout.

"Americans frequently don't bother to do the math and banks know this."

Some probably don't bother but I'd wager many simply cannot do the math at all, or without help from a calculator.

...many Americans cant even comprehend why other countries would use different currencies so the whole issue of currency conversion is baffling to them.

@Toby - Ain't that the truth. I still remember having to deal with a passenger complaint from an American that was somehow offended when they tried to pay in "Nigeria dollars" for something priced in US Dollars and then got offended that we were "discriminating against Americans". If something costs $100, that is 50000 Naira. You can't try to pay 100 Naira instead of $100 and claim you are being discriminated against!!!

The number of folks here defending or finding random anecdotes about why DCC is better is astounding. Just show how folks aren’t financially educated. Idk, unless you have some backwards sketchy bank in a NON-us friendly country then maybe in specific cases dcc comes out ahead. But 99.9% of the time don’t choose dcc.

But then again who cares, when folks willing to pay 8 dollars for a cup of latte at starbucks, they...

The number of folks here defending or finding random anecdotes about why DCC is better is astounding. Just show how folks aren’t financially educated. Idk, unless you have some backwards sketchy bank in a NON-us friendly country then maybe in specific cases dcc comes out ahead. But 99.9% of the time don’t choose dcc.

But then again who cares, when folks willing to pay 8 dollars for a cup of latte at starbucks, they can afford to lose few dollars on a trip as well. These tactics are making a killing.