There are a lot of misconceptions about how credit scores are calculated. When I explain to people that I have 20+ credit cards open at a given time, the first question I’m usually asked is “doesn’t that ruin your credit score?!”

The answer is no, and that in many cases it can actually improve your credit score. But it’s very difficult for that to “click” with people. So I figured I’d explain in more detail, in part by sharing my own credit score as of last week.

Here’s my credit score

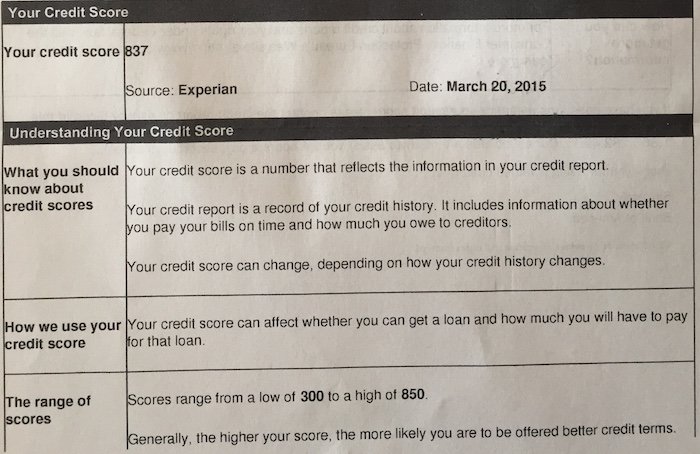

As is the norm when you receive your new card, I received a notice recently containing my credit card and an explanation of my credit.

So what’s my credit score? Well, my Experian credit score is 837 (on a scale of 300 to 850), and better than 98% of US consumers.

So, what’s the secret to a good credit score?

In my “Beginner’s Guide To Miles & Points” I have a section entitled “Credit Cards And Credit Scores.”

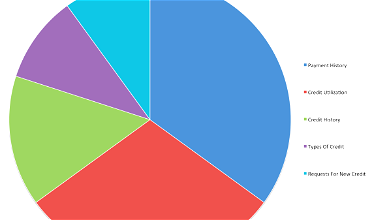

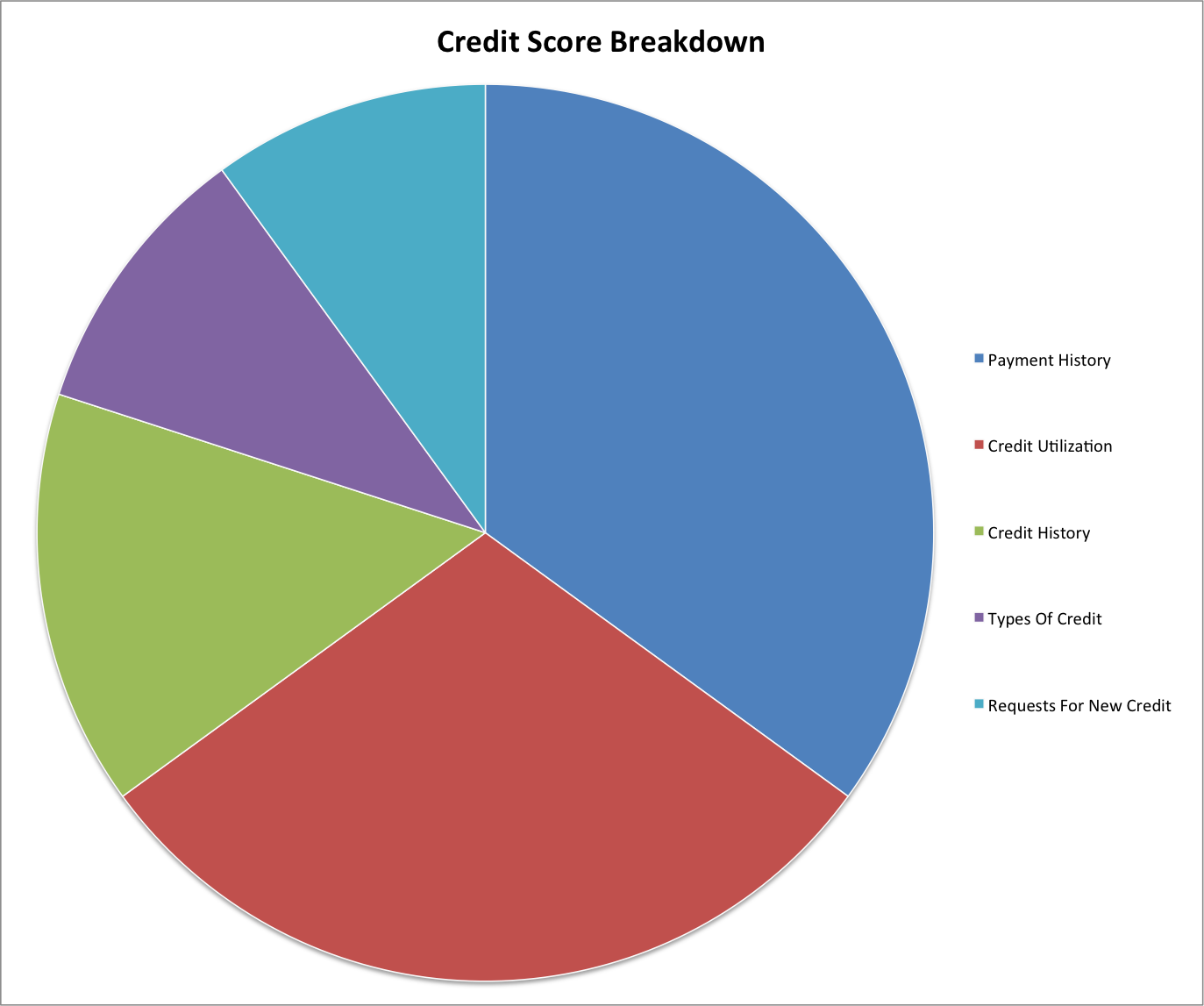

If you haven’t read it I’d suggest checking it out. To summarize, here’s what factors into your credit score:

- 35% of your score is made up of your payment history

- 30% of your score is your credit utilization

- 15% of your score is your credit history

- 10% of your score is made up of the types of credit you use

- 10% of your score is your request for new credit

So how do I have near perfect credit score despite having a huge number of open credit cards and applying for quite a few cards? Here are a few tricks that people easily overlook and/or can’t fully wrap their heads around.

Always make payments on time

35% of your credit score is made up of your payment history. That couldn’t be easier. Just pay your bills on-time and you’ll basically get “perfect marks” for a third of your credit score. If you’re going to be involved in this hobby you’ll want to be well organized, which isn’t a lot of work, really. Just make sure you have payment due dates in your calendar, and have payment alerts set up.

Not only will you be hit with fees for making late payments, but your credit score will also be hit.

Keep your credit utilization low

30% of your credit score is made up of your credit utilization. This simply refers to what percentage of your overall credit you’re using.

Let me give an example. Say you have 10 credit cards, and have a $10,000 credit line on each. That means you have $100,000 of available credit. If you spend $90,000 on your cards each month, you’re utilizing 90% of your credit. That looks risky to the banks, because they start to wonder if you’re getting close to charging things you can’t actually pay for

Conversely, if you have $100,000 of available credit but only spend $1,000 per month, you’re only utilizing 1% of your credit. If you apply for new credits, the banks view you as low risk. Because you’re clearly not trying to max out your credit lines.

So it actually helps to have a lot of cards, so that your overall available credit is high, while your utilization is very low.

And there’s one other trick here — pay your credit card statements before the statement even closes. In other words:

- Say the closing date for a credit card is April 1

- The payment due date is usually a few weeks after that

- I simply pay my credit card bill two days before the statement even closes (in this case, March 30)

- That’s because what’s being reported to the credit bureaus is your utilization at the time your statement closes; so even if my credit line is $10,000 and I spend 90% of that, if I pay off the balance before the statement even closes, then the utilization shows as 0%

Keep some cards for a long time

15% of your credit score is made up of your credit history. One thing that largely factors into this is your average age of accounts.

In other words, the issuers want to see that you’ve been using credit consistently and responsibly for a long time. After all, if you’ve never had a credit card before and then suddenly get five at once, they’re not sure if you’ll be able to handle your credit responsibly.

So while I apply for a lot of new cards, it’s important to also keep some cards long term. This is why I highly recommend a combination of valuable cards that are worth paying annual fees on, as well as no annual fee cards which add value as well.

For example, I consistently hold onto the following cards:

- Chase Sapphire Preferred® Card — this is my primary card, as I earn 3x points on dining, 2x points on travel, get foreign transaction fees waived, and have primary CDW auto rental coverage

- Chase Freedom FlexSM — this is a great no annual fee credit card which offers 5x points in rotating quarterly categories, which I can combine with the Ultimate Rewards points I earn on the Chase Sapphire Preferred

- Hilton Honors American Express Surpass® Card — this card gets me Hilton Honors Gold status for as long as I have the card, which is worth a lot to me, since it gets me free breakfast/club lounge access; Hilton is my backup hotel chain after Hyatt

- IHG One Rewards Premier Credit Card — I receive an annual free night certificate (capped at 40,000 points per night) each year along with IHG Rewards Club Platinum status for as long as I have the card, which more than justifies the annual fee

- The Platinum Card® from American Express — this card is worth it to me for the perks, including an annual airline fee credit, lounge access benefits and bonus spend on airfare

In other words, while the above in some cases represent high annual fees, I’m always getting more value out of the card than what I’m paying for it. And that also helps my credit score.

That’s 80% of your credit score right there

The above alone accounts for 80% of your credit score. And if you play your cards right (no pun intended) your score could actually be higher if you have a lot of cards than if you only have a few cards.

The last 20% of your credit score is made up of a combination of the types of credit lines you use and your requests for new credit. The former refers to having diversified credit lines (credit cards, mortgages, etc.) — the more variety you have, the better.

The only part of your credit score that will negatively be impacted by applying for new cards is your requests for new credit, whereby your score will be temporarily hit by a few points for the inquiry. After 24 months that falls off your report, though, and you’ll just reap the positive benefits of having a lot of cards.

Bottom line

I’m sure most of you already knew that applying for lots of credit cards doesn’t necessarily hurt your credit score, and in many cases even helps it. Though hopefully you can also link your friends & family that are “doubters” of this hobby to this post, so they can see how credit scores actually work in practice.

I doubt I’d have a score of 837 if I didn’t have as many cards as I do, so overall this hobby hasn’t just rewarded me with greatly discounted premium travel, but has actually improved my credit score as well.

If I have a 0% interest for purchases for 6 months, what should my utilisation at the end of each month be then?

From the above, I should aim to keep it at 10% every month. Am I correct? Does that mean that if I use 70% of my balance over3 months and if I even don't pay any interest, my credit score will be reduced?

@ Alvin -- When you take out a 0% interest offer then your credit utilization is whatever percent of your credit line you're using. So if you have a $20,000 credit card and have a 0% interest offer on $10,000, then you'd be utilizing 50% of your credit. So in general that's not great for your credit score.

i think there is some misinformation about leaving a small balance.

it is better to pay off every month.

here is an advise from experian.

"Ideally, you should keep the credit cards open. Use at least one of the cards to make small purchases each month. However, you should not carry a balance. Instead, pay off the charges each month so that you don’t carry a balance from one pay period to the...

i think there is some misinformation about leaving a small balance.

it is better to pay off every month.

here is an advise from experian.

"Ideally, you should keep the credit cards open. Use at least one of the cards to make small purchases each month. However, you should not carry a balance. Instead, pay off the charges each month so that you don’t carry a balance from one pay period to the next.

Making small purchases will keep the card active and keep your balance well below your credit limit. This demonstrates that you consistently manage debt well and can add positive points to your credit scores. Paying the balance in full will prevent paying interest or finance charges on revolving balances.

A combination of using the card but paying off charges to maintain a zero balance will likely improve your credit scores over time."

@brgr - you are only partly correct. You want less than 10% to report each month for optimal utilization scoring. So you want to let 1 or 2 cards report a small balance, not all of them (also, the credit bureau assesses use per card as well as overall use, so keep it below 10% per card as well). If you pay them all off before the statement due date, then it looks like you...

@brgr - you are only partly correct. You want less than 10% to report each month for optimal utilization scoring. So you want to let 1 or 2 cards report a small balance, not all of them (also, the credit bureau assesses use per card as well as overall use, so keep it below 10% per card as well). If you pay them all off before the statement due date, then it looks like you don't use your cards at all and not using them is as bad as running them up to the limits (as far as credit scoring is concerned). They want to see responsible use of credit, not no use.

@Bill N DC did you confirm you were eligible for the bonus? As Lantean hinted at anyone can apply but not anyone gets the bonus.

Every country is different. The above formula apparently does not apply to Australia. In Australia, the frequency of applying credit plays a big part. If you apply 5 cards in a short period of time, you wreck your credit score and will be hard to recover.

I'm a victim of such a system. I have annual income of >$300k on a government permanent job, fully owned my house plus another with no mortgage, paid...

Every country is different. The above formula apparently does not apply to Australia. In Australia, the frequency of applying credit plays a big part. If you apply 5 cards in a short period of time, you wreck your credit score and will be hard to recover.

I'm a victim of such a system. I have annual income of >$300k on a government permanent job, fully owned my house plus another with no mortgage, paid all my bills on time in the last 15 years, but just because I applied 5-6 credits over a period of 6 months (this include signing up a 24 months contract on my new iPhone!), my credit score was dropped to below average. The risk assessment states I'm highly likely to go bankrupt in 12 months. So I can't apply any credit card now.

Stupid system.

Great, informative post!

Good to know, steven k.

Robert D,

2 years ago, i signed up with experian credit service and have been monitoring my credit report almost everyday.

what i can tell you is that chase, amex, BoA and capital one will report the balance at the time of montly closing date.

but US bank will report the balance of last day of each month.

I have read that it doesn't really matter if you pay your bill before the closing date, as your utilization is reported once a month on the same day for all cardholders, regardless of closing date. In other words, the credit card issuer reports all utilization on, say, the 15th of the month. Who knows if that is accurate, however, there's all kinds of conflicting information out there..

So I had an interesting experience with this recently, where I discovered it is NOT advantageous to pay your bills before the due date. My fiancee and I are authorized users on each others cards, which causes all of our credit limit to appear together, at least according to my Equifax report. This resulted in the available credit being well into 6 figures. We usually pay each bill as soon as the statement comes through....

So I had an interesting experience with this recently, where I discovered it is NOT advantageous to pay your bills before the due date. My fiancee and I are authorized users on each others cards, which causes all of our credit limit to appear together, at least according to my Equifax report. This resulted in the available credit being well into 6 figures. We usually pay each bill as soon as the statement comes through. When I looked on my credit report, I found that the number being reported for accounts was often $0, which was destroying our credit utilization, into the low single percents, even though we target in the 7-10% range each month. I realized this was being artificially reduced, based on when we were paying off the accounts and when the balance was being reported. I would actually recommend setting up automatic payments every month a few days before the due date, such that there is no chance that a balance reported is $0. Hope this helps others avoid the same problem I ran in to!

@Bill n DC

are you saying you got approved for another regular AA while you already had one?

i thought we had to wait 18 months, no? thanks.

Hi Lucky!

So are you saying that if my statement balance is $1,000 but my outstanding balance is $1200 then I should go ahead a pay around $1150 so that my next statement prints with only a $50 balance, and that will show a low utilization rate?

@ Daniel -- Yep, you'll want to pay off some of it but not quite all of it. It's good to have a low utilization, but not a zero utilization.

How do you find out your credit score? It seems there alot of companies out there offering credit scores, but I don't know which one to go to! The last credit score I had was in the 700's and I'm just in my mid 20's! :D And I got that score when my bank gave me the results of my limit increase I think it was and it came with the credit score from Equifax.

@ Mike O. -- I'll try to compile a list of which cards offer it as a benefit. In general, though, when you get approved for a card you should get a letter with your credit score on it.

Ben, That strategy works for me, too. Yesterday as I was checking in for a US flt, the web was pushing the citi card, so I applied. I got the call number, so I called. The agent checked, came back on, and said that since I have two other Citi AA cards (Reg & Exec) she could only offer me $7K in credit or she could juggle the credit between cards (I'm a pro with...

Ben, That strategy works for me, too. Yesterday as I was checking in for a US flt, the web was pushing the citi card, so I applied. I got the call number, so I called. The agent checked, came back on, and said that since I have two other Citi AA cards (Reg & Exec) she could only offer me $7K in credit or she could juggle the credit between cards (I'm a pro with Chase on this). Since this hobby only works by paying off balances every month, I said $7K would be fine. ChaChing 50K more AA miles :-)

"I haven't always had good credit, but now that I do....."

Pay your bills!!!! That is the secret of having high credit score. :)

Lucky - what are your plans for the cards that you don't consistently hold on to? For example, the US Airways Mastercard (soon to be AAdvantage Aviator) and AAdvantage Citi Mastercard. Do you cancel before the annual fee hits or try and downgrade to a no AF card? If you aren't able to downgrade, how much does having a few closed accounts of <1 year hurt?

@ Brian -- Generally speaking as long as I have enough "long term" cards I'll just cancel when the annual fee is due again.